Credit Card Statements 2025: Spotting Cash Advance Fees

Anúncios

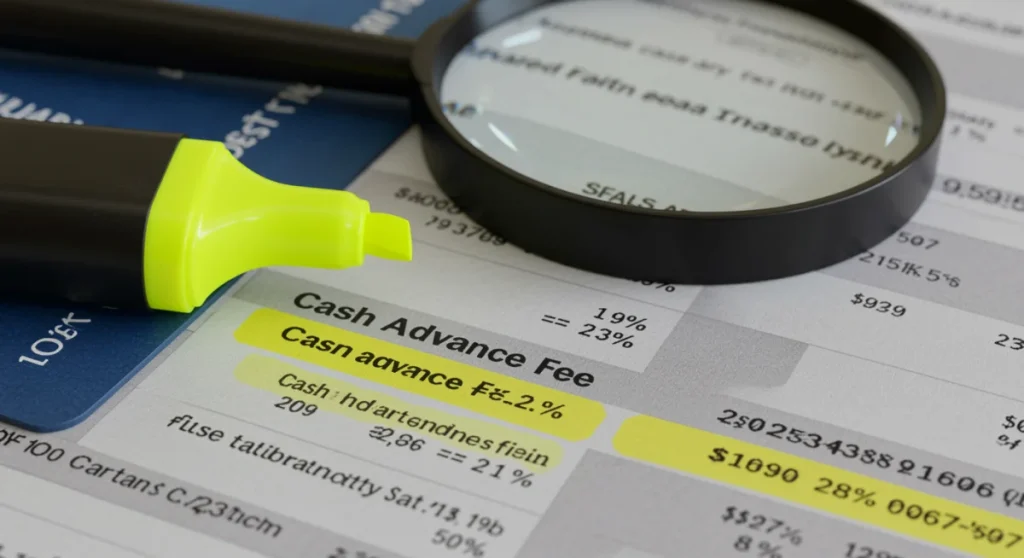

Understanding your 2025 credit card statement is crucial to identify and avoid cash advance fees exceeding 2%, which can significantly impact your financial health.

Anúncios

As we step into 2025, navigating the complexities of your credit card statement has become more critical than ever. For many, the allure of quick cash via a credit card cash advance can mask a significant financial pitfall. This article aims to empower you by providing a comprehensive guide to Decoding the 2025 Credit Card Statement: Identifying Hidden Fees Over 2% on Cash Advances, ensuring you can spot and understand these often-overlooked charges.

Anúncios

The Evolution of Credit Card Fees in 2025

The landscape of credit card fees is constantly evolving, and 2025 brings its own set of nuances that consumers must be aware of. Financial institutions are continually adjusting their fee structures, influenced by economic conditions, regulatory changes, and competitive pressures. Understanding these shifts is the first step towards effective financial management.

While many fees remain standard, such as annual fees or late payment charges, cash advance fees have seen particular attention due to their potential to generate significant revenue for lenders. These fees are often a percentage of the amount advanced, and in some cases, can be a flat fee, whichever is greater. The key is to recognize that these are distinct from the interest charged on the cash advance, which typically begins accruing immediately.

Understanding the Regulatory Environment

Regulatory bodies play a crucial role in shaping how credit card companies can charge fees. In the United States, legislation like the CARD Act of 2009 has provided significant consumer protections, but specific clauses can still allow for substantial cash advance fees. Ongoing discussions and potential new regulations in 2025 might introduce further changes, making it essential for cardholders to stay informed.

- Consumer Financial Protection Bureau (CFPB): This agency oversees financial products and services, including credit cards, and provides resources for consumers to understand their rights and obligations.

- State-Specific Regulations: Some states may have additional laws governing credit card fees, which can vary significantly.

- Cardholder Agreements: Always review your individual cardholder agreement, as it contains the definitive terms and conditions specific to your card.

In conclusion, the fee environment for credit cards in 2025 demands vigilance. Staying updated on regulatory changes and understanding the specific terms of your card agreement are paramount to avoiding unexpected charges, especially those related to cash advances.

Deconstructing Your 2025 Credit Card Statement

Your credit card statement is more than just a bill; it’s a detailed financial document that, when properly understood, can reveal a wealth of information about your spending habits and associated costs. In 2025, statements are designed to be clearer, but the devil is often in the details, particularly when it comes to fees like those for cash advances.

The layout of a typical statement includes sections for new charges, payments, credits, interest charges, and a summary of fees. It’s in the fees section, and sometimes within the transaction details, that cash advance charges are listed. These are often presented as a separate line item, distinct from purchase transactions.

Key Sections to Scrutinize

To effectively identify fees over 2% on cash advances, you need to know exactly where to look. Ignoring these sections can lead to paying more than necessary.

- Summary of Account Activity: This overview often lists total fees charged during the billing cycle.

- Fees and Interest Charged: A dedicated section detailing all fees, including annual fees, late fees, and crucially, cash advance fees. Look for specific labels like ‘Cash Advance Transaction Fee’ or ‘Cash Advance Charge’.

- Transaction Details: Each cash advance transaction will be listed here, sometimes with the fee directly adjacent to it, or indicated by a specific transaction code.

Paying close attention to these sections will allow you to quickly pinpoint any cash advance fees. Remember, the fee amount should be clearly stated, either as a flat amount or as a percentage of the cash advance. Understanding each section of your statement is vital for informed financial decision-making.

Identifying Cash Advance Fees Exceeding 2%

The core of this guide lies in being able to precisely identify when a cash advance fee crosses the 2% threshold. This seemingly small percentage can accumulate rapidly, especially with larger cash advances. It’s not just about seeing a fee listed; it’s about verifying its calculation and understanding its impact.

Credit card companies typically disclose their cash advance fee structure in the cardholder agreement. They might state a fee as ‘either $10 or 5% of the transaction, whichever is greater.’ This means even a small cash advance could incur a significant flat fee that far exceeds 2% of the amount received. For example, a $100 cash advance with a $10 flat fee is a 10% charge.

Calculating the True Cost

To determine if a fee exceeds 2%, you need to do a simple calculation. Divide the cash advance fee by the cash advance amount and multiply by 100. For instance, if you take a $500 cash advance and are charged a $15 fee, that’s ($15 / $500) * 100 = 3%. This clearly exceeds the 2% threshold.

Always cross-reference the fee listed on your statement with the terms outlined in your cardholder agreement. Discrepancies should be immediately questioned with your credit card provider. Being proactive in checking these calculations can save you a substantial amount of money over time.

Common Pitfalls and ‘Hidden’ Aspects of Cash Advance Fees

While some cash advance fees are clearly stated, others can feel somewhat ‘hidden’ due to their immediate application or the way they interact with other charges. It’s essential to be aware of these common pitfalls to avoid unexpected costs that erode your financial stability.

One major aspect is the immediate accrual of interest. Unlike standard purchases, which often have a grace period before interest applies, cash advances typically start accruing interest from the moment the transaction occurs. This means you’re paying a fee to get the cash, and then paying interest on that cash immediately, making it a double hit to your wallet.

Beyond the Transaction Fee

The initial fee is just one component. Several other factors can amplify the cost of a cash advance:

- Higher Interest Rates: Cash advances often carry a significantly higher Annual Percentage Rate (APR) than standard purchases. This elevated rate means the interest accumulates faster and costs you more over time.

- No Grace Period: As mentioned, interest typically starts immediately. There’s no window to pay off the balance without incurring interest, unlike many purchase transactions.

- Impact on Credit Score: While not a direct fee, frequent cash advances can be viewed negatively by credit bureaus, potentially impacting your credit score and future borrowing ability.

Understanding these additional costs and implications allows for a more complete picture of the true expense of a cash advance. It underscores why careful consideration is necessary before resorting to this option, especially when fees exceed the 2% mark.

Strategies for Avoiding High Cash Advance Fees in 2025

Avoiding exorbitant cash advance fees is entirely possible with proactive planning and a clear understanding of your credit card’s terms. The best strategy is often to avoid cash advances altogether, but when circumstances necessitate them, there are ways to minimize the financial impact.

Firstly, always prioritize building an emergency fund. Having readily available savings negates the need for high-cost cash advances. This financial cushion provides a much safer alternative to cover unexpected expenses without incurring additional debt or fees.

Practical Steps to Minimize Fees

If a cash advance is unavoidable, consider these strategies:

- Review Cardholder Agreement: Before taking a cash advance, re-read your agreement to understand the exact fee structure and interest rates applicable. Some cards offer lower fees or introductory rates.

- Consider Alternatives: Explore personal loans, drawing from savings, or even borrowing from friends or family as potentially cheaper alternatives to a credit card cash advance.

- Pay Back Immediately: If you must take a cash advance, pay it back as quickly as possible to minimize the interest accrued. Even a few days can make a difference due to the immediate interest charges.

By implementing these strategies, you can significantly reduce your exposure to high cash advance fees and maintain better control over your credit card debt in 2025. Financial prudence is your best defense against these costly charges.

Disputing Incorrect or Excessive Cash Advance Fees

Despite your best efforts to monitor your statements, you might occasionally encounter a cash advance fee that seems incorrect or excessively high. Knowing how to dispute these charges effectively is a crucial consumer right and can save you money. The process requires clear communication and documentation.

The first step in any dispute is to gather all relevant documentation. This includes your credit card statement, your cardholder agreement outlining the fee structure, and any records of the cash advance transaction itself. These documents will serve as your evidence when communicating with your credit card issuer.

The Dispute Process

Follow these steps to effectively dispute a charge:

- Contact Your Card Issuer: Reach out to your credit card company’s customer service department as soon as you identify the disputed fee. Explain the situation clearly and provide your account details.

- Reference Your Agreement: Point to the specific clauses in your cardholder agreement that you believe the fee violates or that demonstrate an overcharge.

- Document Everything: Keep detailed records of all communications, including dates, times, names of representatives, and summaries of discussions. Follow up written communications with mail, retaining copies for your records.

If the initial contact doesn’t resolve the issue, you can escalate the matter to higher-level customer service or even file a complaint with the Consumer Financial Protection Bureau (CFPB). Being persistent and well-prepared significantly increases your chances of a successful resolution to any disputed cash advance fees.

| Key Aspect | Brief Description |

|---|---|

| Statement Scrutiny | Regularly review your credit card statements, focusing on the ‘Fees and Interest Charged’ section to spot cash advance fees. |

| Fee Calculation | Calculate the percentage of the fee against the cash advance amount to identify charges over 2%. |

| Hidden Costs | Be aware of immediate interest accrual and higher APRs associated with cash advances, beyond the initial fee. |

| Fee Avoidance | Prioritize emergency funds and explore alternatives before resorting to cash advances. Pay back any advance immediately. |

Frequently Asked Questions About 2025 Credit Card Cash Advance Fees

A credit card cash advance fee is a charge imposed by your card issuer when you withdraw cash using your credit card. It’s typically a percentage of the amount withdrawn or a flat fee, whichever is greater, and is separate from the interest that begins accruing immediately.

Look for a section titled ‘Fees and Interest Charged’ or ‘Summary of Account Activity.’ Cash advance fees are usually listed as ‘Cash Advance Transaction Fee’ or similar. They will also appear in the transaction details alongside the cash advance itself.

Many card issuers set a minimum flat fee (e.g., $10). For smaller cash advances, this flat fee can easily translate to a percentage much higher than 2%. Additionally, the APR for cash advances is typically higher and interest accrues instantly, increasing the overall cost.

The best way to avoid these fees is to not take cash advances. If unavoidable, consider alternatives like personal loans or using savings. If you must, pay back the advance as quickly as possible to minimize interest, and always check your cardholder agreement for specific terms.

Immediately contact your credit card issuer’s customer service. Have your statement and cardholder agreement ready. Document all communications, including dates and names. If unresolved, consider escalating the complaint or contacting the CFPB.

Conclusion

Mastering the art of decoding your 2025 credit card statement is an indispensable skill for maintaining financial health. By understanding where and how cash advance fees, especially those exceeding 2%, are presented, you empower yourself to make informed decisions and avoid unnecessary costs. Vigilance, coupled with a proactive approach to managing your credit, ensures that your financial resources are used wisely and not eroded by preventable charges. Stay informed, review your statements meticulously, and always prioritize alternatives to costly cash advances.