Credit Card Delinquency Rates Rise 0.5% in February 2026: States Affected

Anúncios

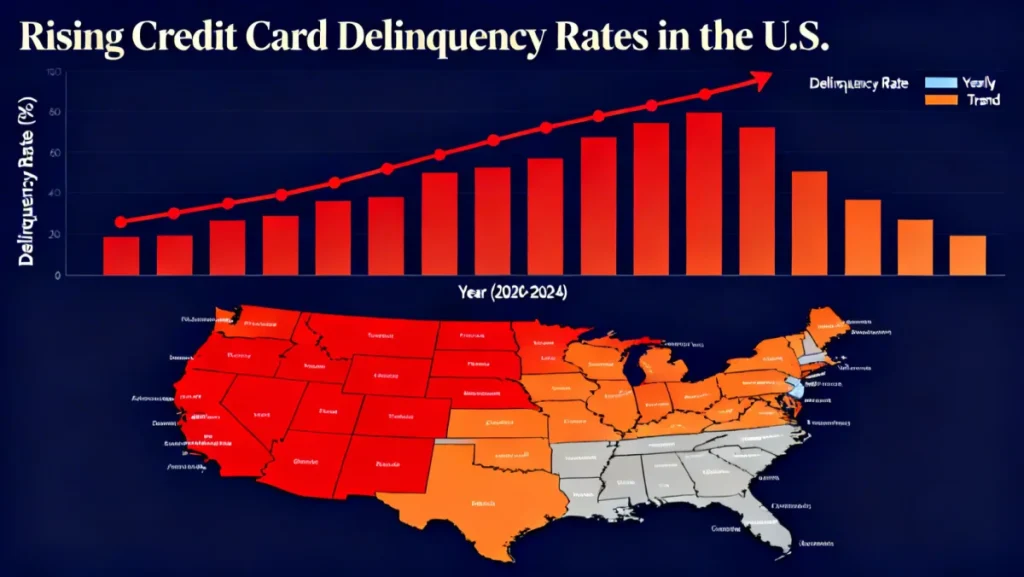

The US experienced a 0.5% increase in credit card delinquency rates in February 2026, indicating heightened economic pressure on consumers and specific states facing more pronounced financial challenges.

Anúncios

The latest financial reports reveal a concerning trend: credit card delinquency rates in the United States climbed by 0.5% in February 2026. This increase, while seemingly modest, signals a broader economic strain impacting households across the nation. Understanding the root causes and identifying the most affected states is crucial for both consumers and financial institutions as we navigate evolving economic landscapes.

Anúncios

Understanding the February 2026 Delinquency Surge

The 0.5% rise in credit card delinquency rates in February 2026 is not an isolated event but rather a symptom of underlying economic shifts. This uptick means more borrowers are falling behind on their credit card payments, typically defined as being 90 days or more past due. Several factors contribute to this trend, creating a complex web of financial pressure on American households.

Economic indicators suggest a confluence of persistent inflation, elevated interest rates, and a softening job market in certain sectors are collectively squeezing consumers’ disposable income. When essential living costs rise, discretionary spending often shrinks, and for many, credit cards become a short-term buffer. However, when these buffers are stretched too thin, delinquencies inevitably follow. Financial analysts are closely monitoring these developments, looking for patterns that might indicate a more widespread financial downturn.

Key Economic Drivers Behind the Increase

- Persistent Inflation: The cost of goods and services remains high, eroding purchasing power.

- High Interest Rates: Elevated federal interest rates translate to higher APRs on credit cards, increasing minimum payments.

- Wage Stagnation: For many, wage growth has not kept pace with inflation, leading to a real decrease in income.

- Job Market Volatility: Specific industries are experiencing layoffs or hiring freezes, creating job insecurity.

The impact of these factors varies regionally, explaining why certain states are feeling the pinch more acutely than others. The interconnectedness of the national economy means that a downturn in one sector or region can have ripple effects, eventually manifesting as increased financial stress for consumers nationwide. This recent rise serves as a critical reminder of the delicate balance in household finances.

Ultimately, the February 2026 delinquency surge underscores the importance of financial vigilance. Consumers are urged to review their budgets, prioritize debt repayment, and seek financial counseling if they find themselves struggling. For lenders, it necessitates a recalibration of risk assessment models and a focus on offering support to at-risk borrowers before their financial situations deteriorate further. This situation demands a proactive approach from all parties involved.

States Bearing the Brunt of Economic Strain

While the national average for credit card delinquency rates saw a 0.5% increase, this figure masks significant regional disparities. Certain states are experiencing a more pronounced surge in delinquencies, indicating localized economic challenges that are hitting their populations particularly hard. These states often share common characteristics, such as reliance on specific industries facing headwinds or higher unemployment rates.

Early data suggests that states heavily dependent on sectors like manufacturing, retail, and hospitality, which have been sensitive to recent economic shifts, are seeing higher delinquency rates. Additionally, states with a higher proportion of residents in lower-income brackets or those with less robust social safety nets may also be more vulnerable. Understanding these geographical concentrations helps in formulating targeted economic relief efforts and financial literacy programs.

Regional Factors Contributing to Higher Delinquency

- Industry Concentration: States with dominant industries experiencing downturns see more job losses and financial instability.

- Cost of Living: Regions where housing and essential services costs are disproportionately high compared to average incomes.

- Demographic Vulnerabilities: Areas with a higher percentage of subprime borrowers or those with limited financial reserves.

For instance, states in the Rust Belt, which have historically faced economic restructuring, are once again showing signs of stress. Similarly, some Sun Belt states, which experienced rapid growth but are now seeing a slowdown, are also reporting increased financial difficulties among their residents. These regional nuances are critical for a holistic understanding of the national economic picture.

Analyzing these state-level trends provides invaluable insights for policymakers and financial institutions. It allows them to tailor interventions, such as unemployment benefits extensions, job retraining programs, or targeted financial aid, to the specific needs of these communities. Ignoring these localized pressures could lead to broader economic instability, making a granular approach essential for recovery and resilience.

The Ripple Effect: How Delinquencies Impact the Broader Economy

A rise in credit card delinquency rates, even a seemingly small one, has a cascading effect throughout the economy. It’s not just about individual struggles; it impacts financial institutions, consumer spending, and ultimately, the overall economic health of the nation. Understanding this ripple effect is crucial for grasping the full implications of the February 2026 data.

For banks and credit card issuers, higher delinquency rates translate to increased loan loss provisions, which can reduce their profitability and potentially tighten lending standards. This tightening can make it harder for other consumers and businesses to access credit, slowing down investment and growth. Furthermore, a decrease in consumer spending, often a consequence of financial stress, can negatively impact retail sales and other sectors of the economy.

Consequences of Widespread Delinquency

- Reduced Lending: Banks become more cautious, making credit less accessible.

- Lower Consumer Confidence: Financial stress leads to decreased spending and investment.

- Increased Bank Losses: Higher charge-offs impact financial institution profitability.

- Economic Slowdown: A cumulative effect of all these factors can contribute to a broader economic contraction.

Moreover, the psychological impact on consumers cannot be overstated. When individuals are burdened by debt and fear of default, their overall sense of financial security diminishes, leading to risk aversion and a reluctance to engage in economic activities that fuel growth. This cycle can be particularly difficult to break once established, highlighting the importance of early intervention.

The February 2026 data serves as an early warning signal that warrants attention from various stakeholders. Proactive measures from government, financial institutions, and consumer advocacy groups can help mitigate the broader economic fallout. Supporting individuals through financial education, debt relief programs, and stable employment opportunities is paramount to safeguarding the economic future.

Consumer Strategies for Navigating Financial Strain

In light of rising credit card delinquency rates, consumers must adopt proactive strategies to safeguard their financial well-being. The current economic climate demands careful budgeting, disciplined spending, and a clear understanding of personal financial obligations. Taking control now can prevent minor financial difficulties from escalating into more serious problems.

One of the most effective strategies is to create a detailed budget, tracking all income and expenses. This allows individuals to identify areas where they can cut back and allocate more funds towards debt repayment. Prioritizing high-interest credit card debt can significantly reduce the overall cost of borrowing and accelerate the path to financial stability. Communication with creditors is also vital if payments become challenging.

Essential Financial Management Tips

- Budgeting: Create and stick to a realistic monthly budget.

- Debt Prioritization: Focus on paying down high-interest debts first.

- Emergency Fund: Build a savings cushion to cover unexpected expenses.

- Credit Monitoring: Regularly check credit reports for errors and signs of fraud.

Another crucial step is to build or bolster an emergency fund. Having savings to cover three to six months of living expenses can provide a critical buffer against unexpected job loss, medical emergencies, or other financial setbacks, reducing the reliance on credit cards for unforeseen costs. This financial safety net is more important than ever in an uncertain economic environment.

For those already struggling, seeking professional help from credit counseling agencies can provide tailored advice and debt management plans. These organizations can negotiate with creditors on behalf of consumers, potentially securing lower interest rates or more manageable payment schedules. Taking these steps empowers consumers to navigate economic strain with greater confidence and resilience, protecting their financial future.

Lender Responses and Policy Implications

The 0.5% rise in credit card delinquency rates in February 2026 is prompting a careful review of lending practices and potential policy responses. Financial institutions are not merely passive observers; they play a critical role in both contributing to and mitigating these trends. Their actions, alongside governmental policies, will shape the future landscape of consumer credit.

Lenders are likely to adjust their risk assessment models, potentially leading to tighter credit standards for new applicants. This could mean higher credit score requirements, lower credit limits, or increased scrutiny of income and debt-to-income ratios. While this might make credit less accessible for some, it is a defensive measure to protect against future losses in a challenging economic environment. Some institutions may also explore offering more flexible payment options or hardship programs for existing customers.

Potential Lender and Policy Adjustments

- Stricter Lending Criteria: Higher credit score requirements and lower credit limits.

- Increased Monitoring: More frequent review of existing customer credit profiles.

- Hardship Programs: Offering payment deferrals or modified payment plans for struggling borrowers.

- Regulatory Scrutiny: Government agencies may increase oversight of lending practices.

From a policy perspective, there could be calls for enhanced consumer protection measures, such as caps on credit card interest rates or more stringent regulations on predatory lending practices. Additionally, governmental stimulus programs or unemployment support could be considered to bolster consumer finances in affected regions. The Federal Reserve will also be closely watching these delinquency trends as it evaluates future monetary policy decisions.

The collaboration between lenders, policymakers, and consumer advocates is essential. Finding a balance between maintaining a healthy credit market and protecting vulnerable consumers is key. Responsible lending practices, coupled with supportive economic policies, can help stabilize credit card delinquency rates and foster a more resilient financial system for all Americans.

Future Outlook: Projections and Preparedness

Looking beyond February 2026, the trajectory of credit card delinquency rates will depend on a complex interplay of economic factors and policy interventions. While the recent increase is a cause for concern, it also presents an opportunity for proactive measures to prevent a more severe downturn. Understanding the potential future outlook allows for better preparedness at both individual and systemic levels.

Economic forecasts vary, but many anticipate that inflation will gradually ease throughout 2026, potentially bringing some relief to consumers. However, interest rates may remain elevated for a period, continuing to impact borrowing costs. The job market’s resilience and wage growth will be critical in determining whether consumers can catch up on their payments and reduce their overall debt burden. Geopolitical events and global supply chain stability will also play a role.

Factors Influencing Future Delinquency Trends

- Inflation Trajectory: How quickly consumer prices stabilize.

- Interest Rate Environment: Future federal reserve policies and their impact on APRs.

- Employment Growth: The strength and stability of the job market.

- Global Economic Health: External factors influencing the US economy.

For individuals, maintaining a strong financial foundation built on savings, a manageable debt-to-income ratio, and a good credit score will be paramount. Diversifying income streams and continuous skill development can also provide a buffer against economic uncertainties. Financial literacy programs will become even more crucial in empowering consumers to make informed decisions.

At a broader level, sustained economic monitoring, agile policy responses, and collaborative efforts between the public and private sectors will be vital. Investing in economic development in vulnerable states, supporting small businesses, and ensuring access to affordable credit are long-term strategies that can foster greater financial resilience. The February 2026 data serves as a call to action for collective preparedness and strategic planning.

| Key Aspect | Brief Description | ||

|---|---|---|---|

| Delinquency Rate Rise | Economic Drivers | Inflation, high interest rates, and wage stagnation are key contributing factors. | |

| Affected States | States reliant on specific industries or with high living costs show greater strain. | ||

| Consumer Strategies | Budgeting, emergency funds, and credit counseling are vital for financial health. |

Frequently Asked Questions About Credit Card Delinquency

A 0.5% rise indicates that a slightly larger percentage of credit card holders are failing to make minimum payments for 90+ days. For the average consumer, it suggests increased financial stress across the economy, potentially leading to tighter credit access and higher borrowing costs in the future.

While specific data varies, states heavily reliant on industries facing downturns, those with higher unemployment, or regions with a disproportionately high cost of living compared to wages, tend to be more affected. These often include parts of the Rust Belt and certain rapidly growing but now slowing Sun Belt regions.

The main factors include persistent inflation eroding purchasing power, elevated interest rates increasing credit card costs, and, in some areas, wage growth that hasn’t kept pace with living expenses. Job market instability in specific sectors also plays a significant role in consumer financial stress.

Consumers can protect their finances by creating and strictly following a budget, prioritizing high-interest debt repayment, building an emergency savings fund, and regularly monitoring their credit reports. Seeking help from non-profit credit counseling agencies is also a valuable option for those struggling.

Lenders are likely to respond by tightening credit standards, potentially requiring higher credit scores or offering lower credit limits for new applications. This may make it harder for some consumers to access credit, and banks might also increase their scrutiny of existing accounts to mitigate risk.

Conclusion

The 0.5% increase in credit card delinquency rates in February 2026 serves as a crucial indicator of underlying economic pressures facing American households. This rise is not merely a statistic; it reflects the real-world impact of inflation, high interest rates, and regional economic disparities on consumers. While certain states are experiencing more acute financial strain, the ripple effects are felt across the national economy, influencing everything from consumer spending to lending practices. Proactive financial management by individuals and responsive strategies from financial institutions and policymakers are essential to navigate this challenging period. By understanding these trends and implementing supportive measures, we can work towards fostering greater financial stability and resilience in the face of evolving economic conditions.