2026 Fed Rate Hikes: 1.5% Impact on US Mortgage Rates

Anúncios

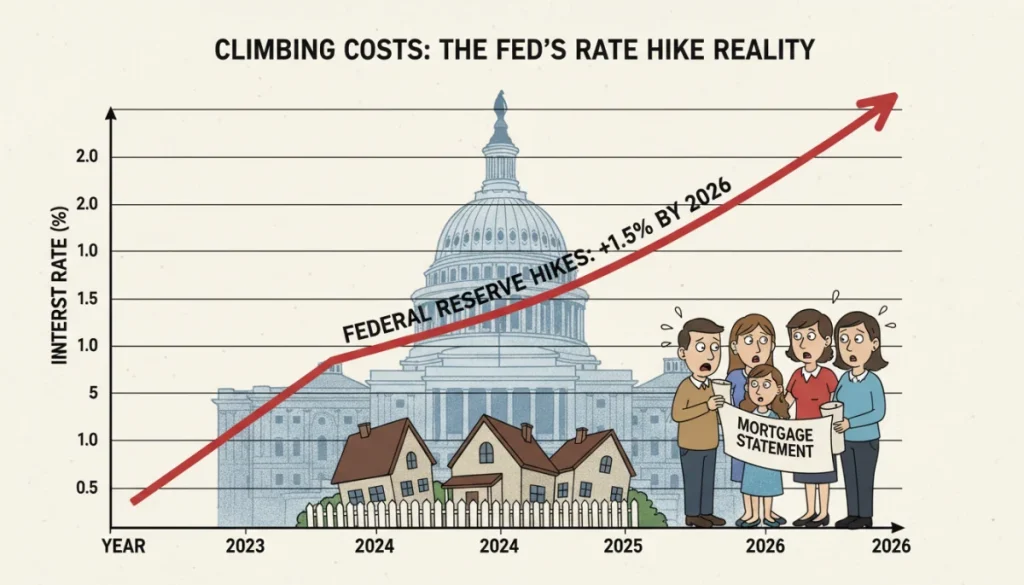

The projected 1.5% Federal Reserve rate hikes in 2026 are poised to significantly increase US mortgage rates, directly affecting affordability for homeowners and prospective buyers.

Anúncios

As we look towards the economic landscape of 2026, one of the most critical factors for American homeowners and prospective buyers is the potential for significant adjustments by the Federal Reserve. Understanding the implications of Navigating the 2026 Federal Reserve Rate Hikes: A 1.5% Impact Analysis on Mortgage Rates for US Homeowners is paramount for financial planning and stability.

Anúncios

Understanding the Federal Reserve’s Role and Rate Hikes

The Federal Reserve, often referred to as the Fed, serves as the central bank of the United States. Its primary mandates include maximizing employment, stabilizing prices, and moderating long-term interest rates. These goals are achieved through various monetary policy tools, with adjusting the federal funds rate being one of the most impactful.

The mechanism of rate adjustments

When the Federal Reserve raises the federal funds rate, it directly influences the cost of borrowing for banks. This, in turn, cascades through the entire financial system, affecting everything from credit card interest rates to auto loans and, most significantly for many Americans, mortgage rates. A 1.5% increase, as projected for 2026, represents a substantial shift in monetary policy.

- Federal Funds Rate: The target rate for interbank lending, influencing broader interest rates.

- Monetary Policy: Actions taken by the Fed to influence the availability and cost of money and credit.

- Economic Stability: The Fed’s dual mandate aims for full employment and price stability (low inflation).

The decision to raise rates is typically a response to inflationary pressures or a robust economy that risks overheating. By making borrowing more expensive, the Fed aims to cool down economic activity, thereby curbing inflation. However, this also has direct consequences for sectors heavily reliant on borrowing, such as the housing market.

In conclusion, the Federal Reserve’s role in setting interest rates is foundational to the US economy. Anticipating a 1.5% increase by 2026 means recognizing a deliberate effort to manage economic growth and inflation, with ripple effects that will be felt across every financial bracket, especially within housing.

Anticipated Economic Conditions Leading to 2026 Rate Hikes

Forecasting economic conditions two years out involves analyzing current trends and projecting their trajectory. Several key indicators typically signal the Federal Reserve’s inclination to adjust interest rates, particularly upward movements. These include inflation rates, employment figures, and overall GDP growth.

Inflationary pressures and labor market strength

Sustained inflation above the Fed’s target of 2% is a primary driver for rate hikes. If consumer prices continue to rise consistently, the Fed will likely act to temper demand. Similarly, a tight labor market, characterized by low unemployment and rising wages, contributes to inflationary pressures as businesses compete for workers and pass on higher costs to consumers.

- Consumer Price Index (CPI): A key measure of inflation, tracking the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

- Unemployment Rate: A low unemployment rate often signals a strong economy, but can also lead to wage inflation.

- Wage Growth: Increases in wages can fuel consumer spending, potentially contributing to inflation.

Beyond these direct indicators, global economic stability and geopolitical events can also play a role. Supply chain disruptions, commodity price shocks, or shifts in international trade policies can all contribute to economic uncertainty or inflationary trends that the Fed would need to address. The 1.5% projection for 2026 suggests a belief in a continued strong economy coupled with persistent, albeit manageable, inflationary forces.

Therefore, the anticipated rate hikes in 2026 are not arbitrary but rather a calculated response to a set of expected economic conditions. These conditions are likely characterized by a resilient economy, a strong job market, and the need to keep inflation in check, ensuring long-term stability.

Direct Impact: How 1.5% Rate Hikes Affect Mortgage Rates

The direct correlation between the federal funds rate and mortgage rates is a critical concept for homeowners and potential buyers. While the federal funds rate doesn’t directly dictate mortgage rates, it significantly influences the cost of funds for lenders, which then translates into the rates offered to consumers.

The mechanism of mortgage rate adjustments

Mortgage rates, particularly for fixed-rate mortgages, are more closely tied to the yield on 10-year Treasury bonds than directly to the federal funds rate. However, the overall interest rate environment set by the Fed heavily influences Treasury yields. A 1.5% increase in the federal funds rate would likely lead to a substantial, though not necessarily identical, increase in mortgage rates.

Consider a scenario where mortgage rates increase by a similar margin. For every percentage point increase in mortgage rates, the monthly payment on a typical home loan can rise significantly. A 1.5% jump could add hundreds of dollars per month to a mortgage payment, making homeownership less accessible for many.

- Fixed-Rate Mortgages: Rates are locked in for the life of the loan, often influenced by 10-year Treasury yields.

- Adjustable-Rate Mortgages (ARMs): Rates fluctuate with a specific index, often tied more directly to short-term rates influenced by the Fed.

- Affordability Index: A measure of whether a typical family can afford the monthly mortgage payments on a median-priced home.

The impact is not uniform. Existing homeowners with fixed-rate mortgages will largely be unaffected unless they plan to refinance. However, those with adjustable-rate mortgages will see their monthly payments increase. New buyers will face higher borrowing costs, potentially reducing their purchasing power and cooling demand in the housing market.

In summary, a 1.5% increase in the federal funds rate in 2026 will undoubtedly translate into higher mortgage rates. This shift will primarily impact new homebuyers and those with ARMs, making home financing more expensive and potentially altering housing market dynamics.

Impact on US Homeowners: Refinancing and Equity

For existing US homeowners, the projected 1.5% Federal Reserve rate hikes in 2026 present a mixed bag of challenges and opportunities, primarily depending on their current mortgage structure and financial goals. The decisions made regarding refinancing, home equity, and overall financial management will be crucial.

Refinancing considerations in a rising rate environment

Homeowners with fixed-rate mortgages secured at lower interest rates will likely find refinancing less appealing as rates climb. The incentive to refinance typically diminishes when current rates are higher than existing ones. However, those with adjustable-rate mortgages (ARMs) might find themselves in a more challenging position, as their monthly payments will increase with the rate hikes.

For ARM holders, careful consideration of their loan terms and the potential for payment shock is essential. Some might explore options to convert to a fixed-rate loan if available, though at a higher rate than previously possible. The goal is to stabilize monthly housing costs amidst fluctuating economic conditions.

- Refinancing Threshold: The point at which current mortgage rates make refinancing financially disadvantageous.

- Payment Shock: A sudden and significant increase in monthly mortgage payments, often experienced by ARM holders.

- Loan Modification: Adjusting loan terms to make payments more manageable, an alternative to refinancing for some.

Furthermore, rising interest rates can affect home equity lines of credit (HELOCs) and home equity loans. These products often have variable interest rates, meaning the cost of borrowing against home equity will increase. This could impact homeowners using HELOCs for renovations, debt consolidation, or other significant expenses.

In conclusion, the 2026 rate hikes will necessitate a review of existing mortgage arrangements for US homeowners. While fixed-rate holders may be shielded, ARM holders and those utilizing home equity products will need to strategize to mitigate increased costs and protect their financial stability.

Impact on Prospective US Homebuyers and Housing Market Dynamics

The projected 1.5% Federal Reserve rate hikes in 2026 will undoubtedly reshape the landscape for prospective US homebuyers, significantly influencing affordability, demand, and overall housing market dynamics. These changes will require strategic planning and adaptation from individuals looking to enter the housing market.

Affordability and purchasing power

Higher mortgage rates directly translate to increased monthly payments for the same loan amount. This reduces the purchasing power of prospective buyers, meaning they can afford less house for the same monthly budget, or they will need to allocate a larger portion of their income to housing costs. This can lead to a slowdown in demand, particularly in price-sensitive markets.

First-time homebuyers, often with tighter budgets, will feel this impact most acutely. The struggle to save for a down payment combined with higher interest rates can push homeownership further out of reach for many, exacerbating existing housing affordability challenges across the nation.

- Debt-to-Income Ratio (DTI): A key metric lenders use to assess a borrower’s ability to manage monthly payments and repay debts. Higher rates can push DTI ratios up.

- Housing Inventory: As demand cools, inventory might increase, potentially alleviating some price pressures but not necessarily affordability.

- Market Cooling: A reduction in overall home sales activity and potentially slower home price appreciation.

The broader housing market will also experience shifts. A decrease in buyer demand due to higher rates could lead to a moderation in home price growth, or even price corrections in some overheated markets. This might offer a silver lining for some buyers, but the increased cost of borrowing could still offset any potential price reductions. Builders might also face challenges with reduced demand and higher financing costs for construction.

Ultimately, the 2026 rate hikes will create a more challenging environment for prospective US homebuyers. They will need to adjust their expectations, potentially compromise on home size or location, or extend their savings period to navigate the new affordability landscape successfully.

Strategies for US Homeowners and Buyers Amidst Rate Hikes

In anticipation of the 2026 Federal Reserve rate hikes, both current US homeowners and prospective buyers must develop robust financial strategies to mitigate potential negative impacts and capitalize on any emerging opportunities. Proactive planning is key to navigating this changing economic climate.

For existing homeowners: review and adapt

Existing homeowners, especially those with adjustable-rate mortgages, should review their loan terms carefully. Understanding when their rates are scheduled to adjust and by how much is crucial. Exploring options like refinancing to a fixed rate, even if it’s higher than their initial rate, might offer long-term payment stability. Additionally, optimizing personal finances, such as paying down other high-interest debts, can free up cash flow to absorb potential mortgage payment increases.

Homeowners with significant equity might consider a cash-out refinance if current rates are still favorable, or explore home equity loans with fixed rates if they need funds for large expenses, locking in a rate before further increases. However, the decision to take on more debt should always be made with caution.

For prospective buyers: prepare and strategize

Prospective buyers need to focus on strengthening their financial position. This includes prioritizing saving for a larger down payment, which reduces the loan amount and thus the impact of higher interest rates. Improving credit scores can also help secure the most favorable rates available. It’s also wise to get pre-approved for a mortgage to understand current affordability and lock in a rate if possible, though pre-approvals typically have a time limit.

- Budget Reassessment: Adjusting personal budgets to accommodate higher potential housing costs.

- Debt Reduction: Lowering existing debt to improve debt-to-income ratios and credit scores.

- Financial Advising: Seeking professional guidance to tailor strategies to individual financial situations.

Furthermore, exploring different types of mortgages, such as FHA or VA loans, which might offer more flexible terms or lower down payment requirements, could be beneficial. Flexibility in location or home type can also expand options as affordability tightens.

In conclusion, preparing for the 2026 rate hikes requires a multi-faceted approach. Homeowners should assess their current loans and equity, while buyers must focus on financial readiness and flexibility. Strategic planning will empower both groups to navigate the evolving housing market effectively.

| Key Aspect | Brief Description |

|---|---|

| Federal Reserve’s Role | Controls monetary policy to influence inflation, employment, and interest rates. |

| 1.5% Rate Hike Impact | Significant increase in borrowing costs, affecting mortgages and other loans. |

| Homeowner Consequences | Higher payments for ARMs, reduced refinancing appeal, increased HELOC costs. |

| Buyer Challenges | Reduced affordability, higher monthly payments, potential cooling of the housing market. |

Frequently Asked Questions About 2026 Rate Hikes

The Federal Reserve typically raises interest rates to combat inflation. By making borrowing more expensive, the Fed aims to slow down economic activity, thereby reducing demand and bringing consumer prices back to a stable level, usually around their 2% target.

If you have a fixed-rate mortgage, a 1.5% rate hike will generally not affect your current payments. However, if you have an adjustable-rate mortgage (ARM), your payments will likely increase after the next scheduled adjustment period, reflecting the new interest rate environment.

If you have an adjustable-rate mortgage or a fixed-rate mortgage significantly higher than current rates, refinancing might be beneficial. Consult a financial advisor to assess your specific situation and determine if locking in a lower fixed rate now makes sense before potential 2026 increases.

Prospective homebuyers should focus on increasing their down payment savings, improving their credit score, and getting pre-approved for a mortgage to understand their current buying power. Exploring different loan types and being flexible with home criteria can also help in a rising rate environment.

Higher mortgage rates typically reduce buyer demand, which can lead to a cooling of the housing market. This might manifest as slower home price appreciation or, in some cases, price adjustments. However, local market conditions and inventory levels will also play significant roles.

Conclusion

The anticipated 1.5% Federal Reserve rate hikes in 2026 represent a significant inflection point for the US housing market and its participants. Both existing homeowners and prospective buyers will need to navigate a landscape characterized by higher borrowing costs and potentially shifting market dynamics. Proactive financial planning, including reviewing current mortgage terms, optimizing personal finances, and strategic saving, will be paramount. While challenges are inevitable, understanding these changes and adapting accordingly will empower individuals to maintain financial stability and make informed decisions in the evolving economic environment.