FTC Guidelines 2026: What Consumers Need to Know

Anúncios

The Federal Trade Commission’s new credit card advertising guidelines, effective March 2026, mandate enhanced transparency and clearer disclosures to protect consumers from deceptive marketing practices.

Anúncios

The financial landscape is constantly evolving, and with it, the need for robust consumer protection. A significant development on this front is the Federal Trade Commission’s (FTC) issuance of new guidelines on credit card advertising, set to take full effect by March 2026. These regulations are poised to redefine how credit card companies communicate with potential customers, placing a strong emphasis on transparency and clarity. Understanding what these changes entail, particularly regarding FTC Issues New Guidelines on Credit Card Advertising by March 2026: What Consumers Need to Know About Transparency, is crucial for every consumer.

Anúncios

Understanding the FTC’s Mandate for Transparency

The Federal Trade Commission (FTC) plays a vital role in protecting consumers from unfair and deceptive business practices. Their latest guidelines for credit card advertising represent a proactive step toward ensuring that individuals can make informed decisions about their financial products. These regulations are not merely bureaucratic hurdles; they are designed to empower consumers by providing a clearer, more honest picture of what they are signing up for.

Historically, the complexity of credit card terms and conditions has often left consumers feeling overwhelmed or misled. The new FTC guidelines aim to rectify this by demanding a higher standard of transparency. This involves not only what information is presented but also how it is presented, ensuring accessibility and comprehensibility for the average person. The core objective is to eliminate ambiguity and prevent predatory marketing tactics.

The Evolution of Consumer Protection

Consumer protection in the credit card industry has seen several iterations, each building upon previous efforts to safeguard individuals. The new FTC guidelines are a response to contemporary advertising challenges and evolving market practices.

- Addressing Digital Advertising: The guidelines specifically tackle the nuances of online and mobile advertising, where information can be easily condensed or hidden.

- Standardizing Disclosures: Aims to create more uniform disclosure formats across different platforms and issuers, reducing confusion for consumers comparing products.

- Combating “Dark Patterns”: Focuses on eliminating deceptive design choices in digital interfaces that manipulate users into making unintended decisions.

Ultimately, this section underscores the FTC’s commitment to creating a fair and equitable marketplace for credit card products. By March 2026, consumers should expect a noticeable shift in how credit card offers are presented, leading to greater clarity and confidence in their financial choices.

Key Changes in Credit Card Advertising Regulations

The forthcoming FTC guidelines introduce several significant changes that will impact both credit card issuers and consumers. These modifications are designed to close loopholes and address areas where previous regulations fell short, particularly concerning clarity and the prevention of misleading claims. Consumers should familiarize themselves with these updates to better navigate the credit card market.

One of the most impactful changes revolves around the presentation of interest rates and fees. Often, promotional rates or deferred interest offers can obscure the true cost of borrowing. The new guidelines mandate that these elements be communicated with unprecedented clarity, ensuring consumers fully grasp the financial implications before committing.

Mandatory Disclosure Enhancements

The FTC is requiring more prominent and understandable disclosures for several critical aspects of credit card agreements. This includes, but is not limited to, annual percentage rates (APRs), fees, and terms related to rewards programs.

- Clearer APR Disclosures: Issuers must prominently display the standard APR, as well as any introductory or penalty APRs, making the transition terms explicit.

- Fee Transparency: All potential fees, such as annual fees, late payment fees, balance transfer fees, and cash advance fees, must be clearly itemized and explained.

- Rewards Program Clarity: Terms and conditions for rewards, points, or cashback programs must be presented in an easy-to-understand manner, including any expiration dates or redemption limitations.

Another crucial area of focus is the advertising of balance transfer offers. While these can be beneficial, the associated fees and the duration of promotional rates are often downplayed. The new rules demand that these details are highlighted, preventing consumers from being surprised by hidden costs or sudden rate increases. These changes aim to foster an environment where consumers can easily compare different credit card products based on transparent and consistent information.

Impact on Consumers: What to Expect by March 2026

For consumers, the implementation of the new FTC guidelines by March 2026 heralds a new era of clarity and protection in the credit card market. The changes are expected to empower individuals with more comprehensive and understandable information, enabling them to make more financially sound decisions. This shift will require a slight adjustment in how consumers evaluate credit card offers, but ultimately, it will be for their benefit.

One of the immediate benefits will be a reduction in the incidence of “bill shock,” where consumers are surprised by unexpected charges or interest rate adjustments. The enhanced disclosure requirements mean that the true cost of a credit card, including all potential fees and interest structures, will be laid out in a much more straightforward manner. This proactive approach aims to prevent financial distress caused by misleading or incomplete information.

Empowering Informed Financial Decisions

The core of the FTC’s initiative is to equip consumers with the tools to make truly informed choices. This goes beyond simply reading the fine print; it’s about making the fine print easily digestible.

- Easier Comparison Shopping: Standardized disclosures will make it simpler to compare different credit card products side-by-side, based on transparent terms.

- Reduced Risk of Debt Traps: Clearer communication about interest rates and payment structures can help consumers avoid falling into cycles of high-interest debt.

- Greater Trust in Advertisements: As misleading claims become less prevalent, consumers can develop more trust in the information provided by credit card issuers.

Furthermore, the guidelines are likely to encourage credit card companies to compete more on the actual value and terms of their products, rather than relying on deceptive marketing. This could lead to a healthier market where innovation focuses on beneficial features and competitive pricing, rather than complex and opaque offers. Consumers should anticipate a more transparent and trustworthy experience when applying for and using credit cards.

How Credit Card Companies Are Adapting to the New Rules

The credit card industry is a dynamic sector, and companies are already beginning to adapt their advertising strategies and internal processes in anticipation of the March 2026 deadline. This adaptation involves a significant overhaul of marketing materials, website content, and even the training of customer service representatives. The goal is not just compliance, but also to build stronger, more transparent relationships with their customer base.

Many issuers are investing in technology to simplify their disclosure processes and ensure that all mandated information is presented clearly and consistently across all platforms. This includes developing user-friendly interfaces for online applications and creating standardized templates for printed materials. The challenge lies in balancing regulatory compliance with effective marketing that still attracts customers.

Operational and Marketing Adjustments

Compliance with the new FTC guidelines requires a multi-faceted approach, affecting various departments within credit card companies.

- Marketing Material Redesign: Advertisements, brochures, and online banners are being revised to prominently feature key terms and conditions, rather than burying them in small print.

- Website and App Overhauls: Digital platforms are being updated to ensure disclosures are easily accessible and understandable, avoiding “dark patterns” that can mislead users.

- Employee Training: Customer service and sales teams are receiving training on the new disclosure requirements to accurately answer consumer questions and provide consistent information.

The shift also encourages a move away from overly aggressive or deceptive sales tactics towards a more consultative approach. Companies that embrace transparency early on may gain a competitive advantage by fostering greater consumer trust and loyalty. This adaptation period is crucial for the industry to align with the FTC’s vision of a more transparent financial marketplace.

The Role of Technology in Ensuring Compliance and Transparency

Technology is playing an increasingly critical role in helping credit card companies meet the stringent new FTC guidelines and in delivering the transparency consumers expect. From automated compliance checks to advanced data analytics, technological solutions are enabling issuers to streamline their processes and ensure accuracy across all advertising channels. This integration of technology is not just about meeting regulatory demands; it’s about enhancing the overall customer experience.

Sophisticated software can now scan marketing materials for compliance with specific disclosure requirements, flagging potential issues before they become public. This proactive approach minimizes the risk of non-compliance and the associated penalties. Furthermore, AI-driven tools can help analyze consumer feedback and engagement with disclosures, providing valuable insights into how information can be made even clearer.

Innovation in Disclosure Delivery

Technological advancements are transforming how disclosures are presented, making them more interactive and user-friendly.

- Interactive Disclosure Tools: Online platforms can offer interactive elements where consumers can click on terms to get detailed explanations or see examples of how fees are applied.

- Personalized Information: AI can potentially tailor disclosure presentations based on a consumer’s financial literacy level or specific areas of interest, ensuring maximum comprehension.

- Blockchain for Transparency: While nascent, blockchain technology could offer an immutable record of advertised terms, further enhancing trust and verifiability.

Moreover, the use of clear, concise language in digital formats, often guided by content management systems, ensures consistency across all consumer touchpoints. The synergistic relationship between regulatory requirements and technological innovation is driving a significant improvement in the transparency of credit card advertising, ultimately benefiting the consumer.

Preparing for the Future: A Consumer’s Guide to Credit Card Choices

As the March 2026 deadline approaches and the new FTC guidelines take full effect, consumers have an excellent opportunity to re-evaluate their credit card choices and approach new applications with greater confidence. The increased transparency means that the onus is still on the consumer to read and understand the terms, but the information will be presented in a much more accessible format. This is an opportune time to become more financially literate and proactive in managing one’s credit.

It’s important to remember that while the regulations will improve clarity, they don’t replace the need for personal due diligence. Consumers should still compare offers from different issuers, paying close attention to the now-clearer interest rates, fees, and rewards structures. Utilize the new transparency to your advantage, ensuring that any credit card you choose aligns perfectly with your financial goals and spending habits.

Strategies for Smarter Credit Card Management

With enhanced transparency, consumers can adopt more effective strategies for choosing and managing their credit cards.

- Thoroughly Review Disclosures: Take the time to read all provided terms and conditions, especially the summary boxes, which will be more comprehensive.

- Understand APRs and Fees: Be clear on the standard APR, any introductory rates, and all potential fees. Understand how these can impact your overall cost of borrowing.

- Evaluate Rewards Programs Critically: Don’t be swayed solely by flashy rewards. Understand the redemption process, any caps, and whether the rewards truly align with your spending.

- Monitor Your Statements: Regularly check your credit card statements for accuracy and to ensure you understand all charges and interest calculations.

By proactively engaging with the clearer information provided, consumers can avoid common pitfalls and leverage credit cards as powerful financial tools, rather than sources of unexpected debt. The future of credit card advertising, post-March 2026, promises a more level playing field, but an informed consumer remains the best defense against financial missteps.

| Key Aspect | Brief Description |

|---|---|

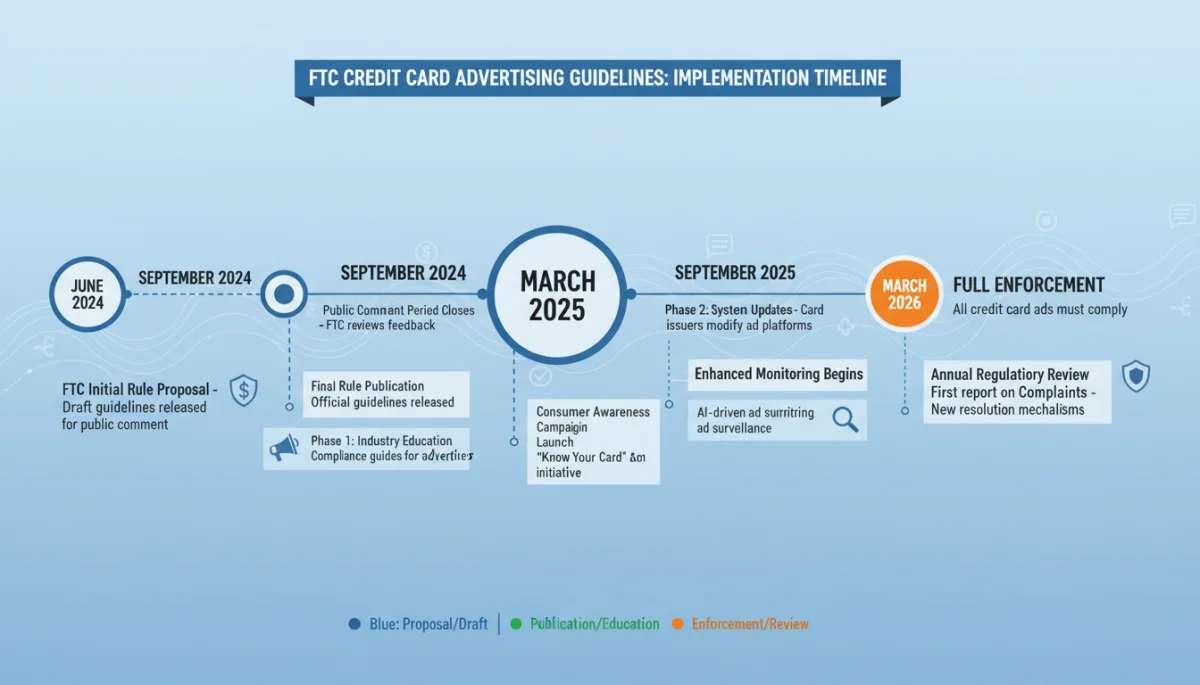

| Effective Date | New FTC guidelines for credit card advertising become mandatory by March 2026. |

| Enhanced Disclosures | Mandates clearer presentation of APRs, fees, and rewards program terms. |

| Consumer Impact | Aims to reduce bill shock and enable more informed financial decisions. |

| Industry Adaptation | Companies are revising marketing, digital platforms, and training for compliance. |

Frequently Asked Questions About FTC Credit Card Guidelines

The primary goal is to enhance transparency in credit card advertising. This means ensuring consumers receive clear, unambiguous information about interest rates, fees, and terms, allowing them to make better-informed financial decisions and protect them from deceptive practices.

The new Federal Trade Commission guidelines for credit card advertising are scheduled to be fully implemented and take effect by March 2026. This allows credit card issuers sufficient time to adjust their marketing strategies and disclosure processes to comply with the new regulations.

The guidelines do not directly change interest rates or fees. Instead, they mandate clearer and more prominent disclosure of these items. Consumers will have a more straightforward understanding of all associated costs, including introductory APRs, penalty rates, annual fees, and other charges, before applying.

Yes, absolutely. The new FTC guidelines specifically address digital advertising, including online banners, social media promotions, and mobile app interfaces. They aim to prevent misleading “dark patterns” and ensure that all necessary disclosures are easily accessible and understandable across all digital platforms.

Consumers should actively review and compare credit card offers, paying close attention to the enhanced disclosures. Utilize the clearer information to understand all terms, conditions, and potential costs. This proactive approach will help in selecting a credit card that best suits individual financial needs and goals.

Conclusion

The FTC’s new guidelines for credit card advertising, effective by March 2026, mark a pivotal moment for consumer protection and transparency in the financial sector. These regulations are designed to strip away ambiguity and ensure that consumers are equipped with clear, comprehensive information before making credit card decisions. While the industry adapts to these changes, consumers stand to benefit significantly from more honest advertising, reduced risk of hidden fees, and an overall more trustworthy marketplace. By understanding these new standards and remaining vigilant, individuals can navigate their credit card choices with greater confidence and make more informed financial decisions for their future.