Credit Card Fees 2026: Annual, Late, and Balance Transfer Impact

Anúncios

The landscape of credit card fees in 2026, encompassing annual, late, and balance transfer costs, significantly influences consumer financial health, demanding careful understanding and strategic management to mitigate their impact.

Anúncios

Understanding the impact of credit card fees in 2026 is more crucial than ever for American consumers. These charges, which include annual, late, and balance transfer costs, can subtly erode your financial well-being if not managed proactively. As the financial landscape evolves, staying informed about these potential pitfalls is the first step towards smarter credit card usage and greater financial stability.

Anúncios

The Evolution of Annual Credit Card Fees

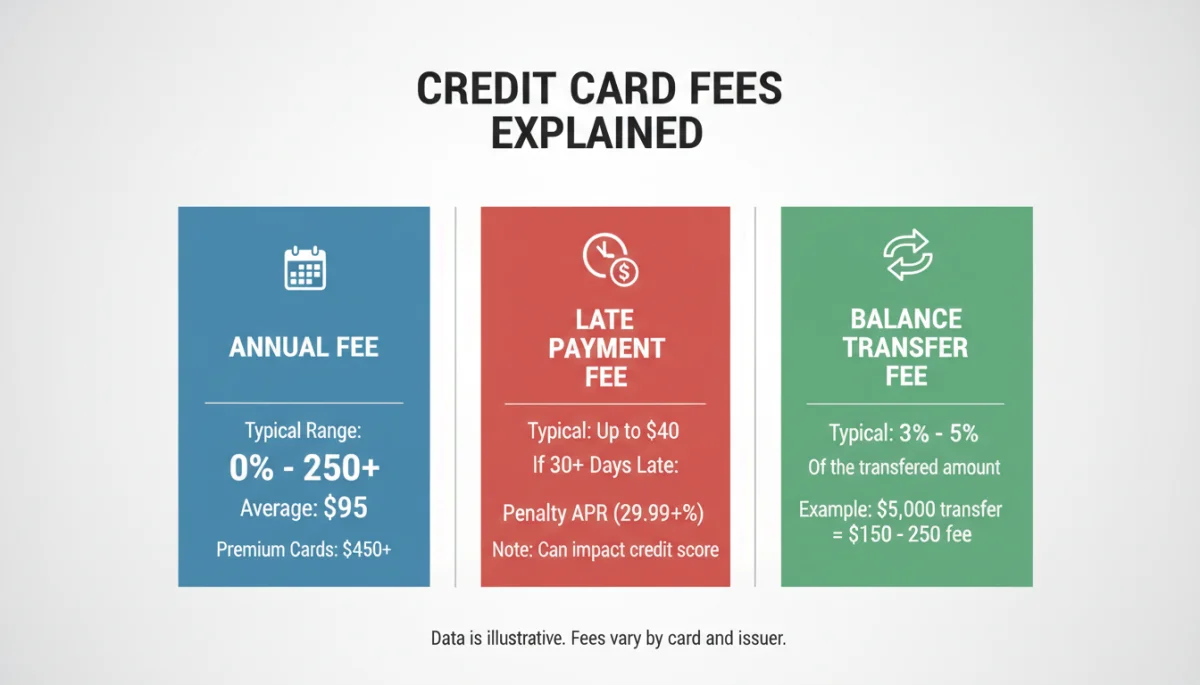

Annual fees, a recurring charge for the privilege of holding certain credit cards, have been a subject of increasing scrutiny. In 2026, these fees continue to vary widely, primarily dependent on the card’s benefits, rewards program, and perceived prestige. While some cards offer substantial perks that might justify a higher annual fee, others may impose fees that outweigh the benefits for the average consumer.

It is essential for cardholders to regularly evaluate whether the value received from a card, such as travel rewards, cash back, or exclusive access, truly compensates for its annual cost. The market in 2026 sees a growing trend of premium cards with elevated annual fees, often marketed towards high-spenders or those seeking luxury travel experiences.

Premium Card Fees vs. Standard Options

Premium credit cards, often boasting extensive travel insurance, airport lounge access, and concierge services, typically come with annual fees ranging from $95 to over $500. Conversely, many standard and cash-back cards maintain no annual fee, making them attractive for consumers who prioritize simplicity and cost-avoidance.

- High-tier benefits: Exclusive travel perks, increased rewards rates, and comprehensive insurance coverage.

- Mid-tier options: Moderate annual fees, balanced with solid rewards and some travel benefits.

- No-annual-fee cards: Ideal for everyday spending, building credit, or consumers who do not maximize premium perks.

The decision to pay an annual fee should always stem from a clear understanding of your spending habits and how well they align with the card’s offerings. A card with a $99 annual fee might be a bargain if you consistently utilize its benefits, but a financial drain if it sits unused in your wallet.

In conclusion, annual fees are a fundamental aspect of many credit card offerings in 2026. Consumers must critically assess the value proposition of any card with an annual fee, ensuring that the benefits genuinely offset the cost. Ignoring this assessment can lead to unnecessary expenses that detract from your financial goals.

Navigating the Landscape of Late Payment Fees

Late payment fees remain a significant concern for credit card users in 2026. These penalties are levied when a cardholder fails to make the minimum payment by the due date. The primary purpose of these fees is to encourage timely payments and compensate the issuer for the increased risk and administrative costs associated with delinquent accounts.

While federal regulations, such as the CARD Act, have placed some limits on how high these fees can be, issuers still have considerable leeway. The exact amount can vary based on the card agreement and the cardholder’s payment history. Repeated late payments not only incur fees but can also lead to a higher Annual Percentage Rate (APR) and a negative impact on your credit score.

Typical Late Fee Structures

Most credit card issuers in 2026 implement a tiered structure for late fees. The first late payment might incur a fee, with subsequent late payments within a certain period potentially leading to higher charges. Furthermore, some issuers may impose a penalty APR, which is a significantly higher interest rate applied to your outstanding balance, sometimes indefinitely.

- First late payment: Often a fixed amount, typically around $30-$40, depending on the outstanding balance.

- Subsequent late payments: Can be higher, sometimes reaching $41 or more, especially if within six billing cycles.

- Penalty APR: Activation of a much higher interest rate on your entire balance, making debt repayment more challenging.

The best strategy to avoid late fees is to establish robust payment reminders, whether through calendar alerts, automatic payments, or mobile banking notifications. Even a single late payment can set off a chain reaction of negative financial consequences, making vigilance paramount.

In summary, late payment fees are a preventable expense that can significantly impact your financial health. Understanding their structure and implementing proactive payment management strategies are crucial steps for any responsible credit card user in 2026.

Understanding Balance Transfer Fees in 2026

Balance transfer fees are a common charge associated with moving debt from one credit card to another, typically to take advantage of a lower or introductory 0% APR. While balance transfers can be an excellent tool for debt consolidation and interest savings, the fees involved can sometimes negate a portion of these benefits if not carefully considered.

In 2026, the standard balance transfer fee usually ranges from 3% to 5% of the transferred amount. This fee is typically applied at the time of the transfer, adding to the total debt. For example, transferring a $10,000 balance with a 3% fee would immediately add $300 to your debt, making your new balance $10,300.

Calculating the Cost-Benefit of a Balance Transfer

Before initiating a balance transfer, it is crucial to perform a cost-benefit analysis. Compare the balance transfer fee against the interest you would save by moving your debt to a lower APR card. A 0% introductory APR offer, even with a 3-5% fee, often presents significant savings over a high-interest rate card, particularly for larger balances.

- Identify high-interest debt: Pinpoint which credit cards carry the highest interest rates.

- Research transfer offers: Look for cards with competitive introductory 0% APR periods and reasonable balance transfer fees.

- Calculate total savings: Factor in the balance transfer fee against the interest saved over the promotional period.

It’s also important to note any restrictions or conditions associated with balance transfer offers, such as a limited time frame to complete the transfer after account opening. Missing these deadlines can result in the standard APR being applied, diminishing the value of the transfer.

Ultimately, balance transfer fees are a necessary consideration when using this debt management strategy. By meticulously calculating the costs and benefits, consumers can leverage balance transfers effectively to reduce their overall debt burden in 2026.

Hidden and Lesser-Known Credit Card Fees

Beyond the more prominent annual, late, and balance transfer fees, credit cards in 2026 can come with a variety of other charges that might surprise unsuspecting cardholders. These ‘hidden’ fees, while often smaller individually, can accumulate and significantly impact your financial standing over time if ignored.

One common example is the foreign transaction fee. Many cards charge 1% to 3% on purchases made outside the United States or in foreign currencies. For frequent international travelers or online shoppers who buy from overseas retailers, these fees can quickly add up. Opting for a card with no foreign transaction fees is a smart move for such individuals.

Another often overlooked fee is the cash advance fee. When you use your credit card to get cash, whether from an ATM or a bank, you’re typically charged a fee (often 3% to 5% of the amount) and start accruing interest immediately, often at a higher APR than regular purchases. This makes cash advances an expensive form of borrowing that should be avoided unless absolutely necessary.

Other Fees to Watch Out For

Several other fees, though less common, can still affect specific cardholders. These include:

- Over-limit fees: Charged if you exceed your credit limit, though many cards have eliminated these or require opt-in consent.

- Returned payment fees: Incurred if a payment you make is returned due to insufficient funds.

- Expedited payment fees: Some issuers charge extra to process a payment quickly, often over the phone or online, to avoid a late fee.

- Inactivity fees: While rare, some older or less common cards might charge a fee if the account remains unused for an extended period.

Thoroughly reviewing your cardholder agreement and understanding all potential fees is crucial. Many of these charges can be avoided with careful planning and responsible card usage. Being aware of these lesser-known fees helps consumers make more informed decisions about their credit card choices and usage patterns in 2026.

In essence, credit card statements can reveal more than just your spending; they can highlight various charges that impact your financial health. Proactive research and understanding are your best defenses against these often-overlooked costs.

Strategies for Minimizing Credit Card Fees in 2026

Effectively managing credit card fees in 2026 requires a proactive approach and a clear understanding of your financial habits. Minimizing these costs can significantly improve your financial health, freeing up more of your income for savings or other investments. The key lies in strategic card selection, diligent payment practices, and continuous monitoring of your accounts.

One fundamental strategy is to choose credit cards that align with your spending and lifestyle. If you travel frequently, a card with no foreign transaction fees and travel rewards might justify an annual fee. Conversely, if you prioritize simplicity and avoid debt, a no-annual-fee card with a low APR for purchases could be more suitable.

Practical Tips to Reduce Fee Exposure

Several actionable steps can help you keep credit card fees at bay:

- Pay on time, every time: Set up automatic payments or calendar reminders to avoid late fees. Even paying the minimum on time is better than incurring a penalty.

- Avoid cash advances: These are almost always an expensive form of borrowing due to immediate fees and high interest rates.

- Monitor your statements: Regularly review your credit card statements for any unfamiliar charges or fees you weren’t expecting.

- Negotiate annual fees: If you have a good payment history and a strong relationship with your issuer, you might be able to negotiate a waiver or reduction of an annual fee, especially if you’re considering closing the account.

- Utilize balance transfers wisely: If using a balance transfer, ensure you can pay off the transferred amount before the promotional 0% APR period ends to maximize savings.

Furthermore, consider setting up alerts for approaching due dates or when your balance approaches your credit limit. Many issuers offer these services for free, providing an extra layer of protection against unexpected fees. By integrating these strategies into your financial routine, you can significantly reduce the impact of credit card fees.

In conclusion, minimizing credit card fees is an achievable goal through informed choices and diligent financial practices. Taking control of your credit card usage not only saves you money but also strengthens your overall financial resilience in the evolving economic landscape of 2026.

Regulatory Changes and Consumer Protection in 2026

The regulatory environment surrounding credit card fees is dynamic, with ongoing efforts to balance consumer protection with the operational needs of financial institutions. In 2026, consumers can expect the existing frameworks, primarily shaped by acts like the CARD Act of 2009, to continue influencing how fees are disclosed and applied. However, new legislative discussions and technological advancements may introduce subtle shifts in consumer protections.

Regulators are consistently evaluating the fairness and transparency of credit card practices. This includes examining the clarity of fee disclosures, the reasonableness of fee amounts, and the accessibility of information for consumers to make informed decisions. The aim is to prevent predatory practices and ensure that consumers are not unfairly burdened by unexpected charges.

Key Areas of Regulatory Focus

Several aspects of credit card fees remain under the close watch of consumer protection agencies:

- Transparency in disclosures: Ensuring that all fees, especially annual, late, and balance transfer fees, are clearly communicated to cardholders before they commit to an agreement.

- Reasonableness of fee amounts: Scrutinizing whether fee amounts are proportionate to the costs incurred by the issuer or if they serve primarily as profit centers.

- Impact on vulnerable populations: Assessing how fees disproportionately affect low-income individuals or those with limited financial literacy.

Advocacy groups continue to play a vital role in pushing for stronger consumer protections, particularly concerning fees that can trap individuals in cycles of debt. While a complete overhaul of credit card fee regulations might not occur in 2026, incremental changes and stricter enforcement of existing rules are plausible.

For consumers, staying informed about these regulatory shifts is beneficial. Awareness of your rights and the protections in place can empower you to challenge unfair fees and choose credit products that align with your financial goals. The ongoing dialogue between regulators, industry, and consumer advocates ensures that the credit card landscape continues to evolve with consumer interests in mind.

Ultimately, the regulatory framework in 2026 seeks to foster a more equitable and transparent credit card market. By understanding these protections, consumers can navigate the complexities of credit card fees with greater confidence and security.

| Key Fee Type | Brief Description |

|---|---|

| Annual Fee | A yearly charge for holding certain credit cards, often tied to premium benefits. |

| Late Payment Fee | Incurred when minimum payment is not received by the due date, potentially leading to higher APR. |

| Balance Transfer Fee | A charge (typically 3-5%) for moving debt from one credit card to another. |

| Foreign Transaction Fee | A percentage charge on purchases made outside the U.S. or in foreign currencies. |

Frequently Asked Questions About Credit Card Fees

To avoid annual fees, choose credit cards that explicitly state ‘no annual fee.’ Alternatively, for cards with fees, actively use the benefits (like travel rewards or cash back) to ensure their value exceeds the fee. You can also try negotiating with your issuer for a fee waiver if you have a strong payment history and good credit.

If you make a late payment, you will typically incur a late fee. Repeated late payments can also lead to a penalty APR, where your interest rate significantly increases. Furthermore, late payments can negatively impact your credit score, making it harder to obtain favorable terms for future loans or credit.

Balance transfer fees are not always worth it; it depends on your specific situation. They are most beneficial if you have high-interest debt and can pay off the transferred balance before the introductory 0% APR period ends. Always calculate the total fee versus the interest saved to determine if it’s a cost-effective strategy for you.

Foreign transaction fees are charges, typically 1% to 3% of the purchase amount, applied to transactions made in a foreign currency or outside your home country. To avoid them, use a credit card specifically advertised as having ‘no foreign transaction fees’ when traveling internationally or making online purchases from overseas merchants.

While most credit card fees themselves don’t directly impact your credit score, the behaviors that lead to them often do. For instance, late payment fees result from late payments, which are reported to credit bureaus and negatively affect your score. High annual fees, if they lead to increased credit utilization, could also indirectly impact your score.

Conclusion

The intricate world of credit card fees in 2026 demands a well-informed and strategic approach from consumers. From annual charges that unlock premium benefits to late payment penalties and balance transfer costs, each fee carries its own financial implications. By understanding these various charges, actively monitoring your accounts, and adopting responsible credit card habits, you can significantly mitigate their impact on your personal finances. Staying abreast of regulatory changes and leveraging available consumer protections further empowers individuals to navigate the credit card landscape with confidence, ensuring that credit remains a tool for financial growth rather than a source of unexpected expenses.