Credit Card Debt Consolidation 2026: Reduce Payments by 20%

Anúncios

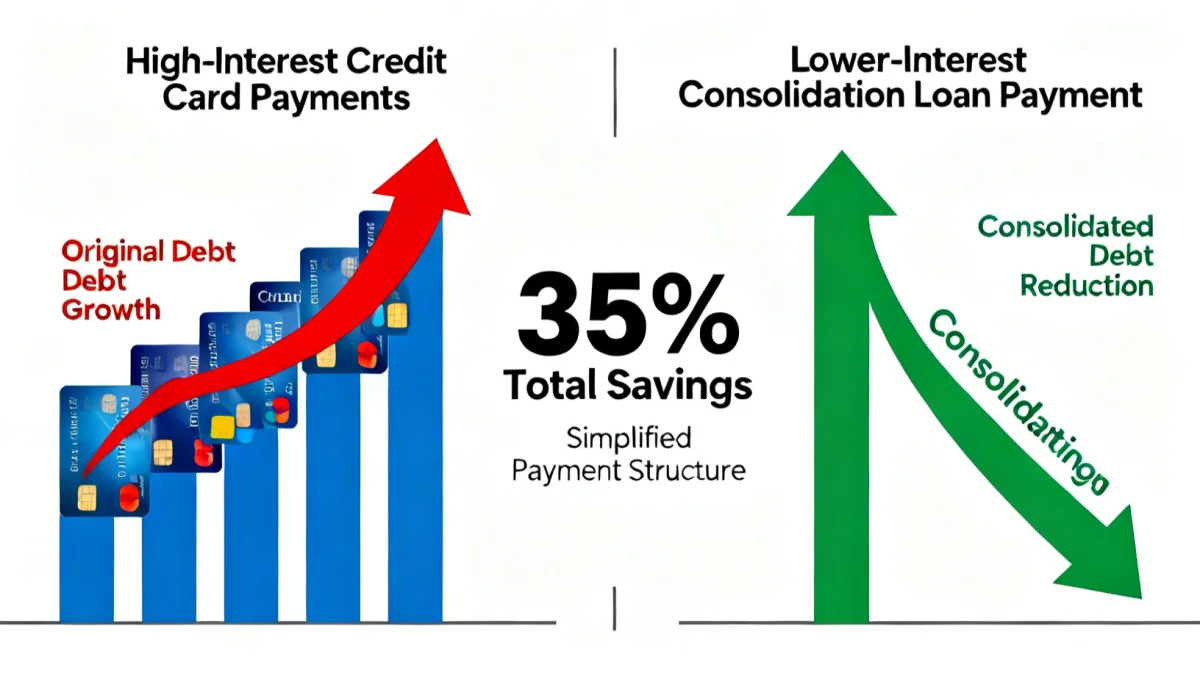

Credit card debt consolidation in 2026 offers a strategic financial solution for individuals aiming to simplify their finances and reduce monthly payments by at least 20%, often through lower interest rates or extended repayment terms.

Anúncios

Are you feeling overwhelmed by mounting credit card balances and high-interest rates? The prospect of achieving financial stability can seem distant, but there’s a powerful tool available: credit card debt consolidation in 2026. This strategy could be your key to simplifying your finances and potentially reducing your monthly payments by a significant 20% or more. Let’s explore how this can be a game-changer for your financial future.

Anúncios

Understanding Credit Card Debt Consolidation

Credit card debt consolidation is a financial strategy designed to combine multiple high-interest credit card debts into a single, more manageable payment. The primary goal is often to secure a lower interest rate, which can significantly reduce the total amount paid over time and make monthly payments more affordable. This approach streamlines your financial obligations, turning several due dates and varying interest rates into one clear, consistent payment.

In 2026, with evolving financial landscapes and new product offerings, understanding the nuances of consolidation is more crucial than ever. It’s not just about bundling debts; it’s about strategically leveraging financial instruments to gain control and accelerate your path to debt freedom.

The Core Mechanism: How It Works

At its heart, consolidation involves taking out a new loan or using an existing financial product to pay off all your smaller, high-interest debts. This new financial product typically comes with a lower interest rate or more favorable terms. The goal is to replace several challenging payments with one simpler, often cheaper, payment.

- Simplified Payments: Instead of juggling multiple credit card bills, you have one single payment each month.

- Lower Interest Rates: Often, consolidation loans or balance transfer cards offer significantly lower interest rates than traditional credit cards.

- Fixed Repayment Schedule: Many consolidation options come with a clear, fixed repayment timeline, providing a definitive end date for your debt.

- Potential for Savings: Reducing interest means more of your payment goes towards the principal, saving you money in the long run.

Ultimately, credit card debt consolidation in 2026 is about creating a clearer, more efficient pathway out of debt. By understanding its mechanics, consumers can make informed decisions that align with their financial goals and lead to substantial savings.

Types of Consolidation Options Available in 2026

The financial market in 2026 offers several avenues for debt consolidation, each with its own advantages and considerations. Choosing the right option depends on your credit score, the amount of debt you have, and your financial goals. It’s essential to evaluate these options carefully to find the best fit for your situation, ensuring you maximize your chances of reducing monthly payments by 20% or more.

Navigating these choices requires a clear understanding of what each product entails and how it impacts your overall financial health. The landscape of financial products is always evolving, so staying informed about the latest offerings is key.

Personal Loans for Debt Consolidation

One of the most popular methods, a personal loan allows you to borrow a lump sum and use it to pay off your credit card debts. These loans typically come with fixed interest rates and repayment terms, offering predictability. Lenders in 2026 are increasingly offering competitive rates for those with good credit scores, making them an attractive option.

- Predictable Payments: Fixed monthly installments make budgeting easier.

- Lower Interest Rates: Often significantly lower than credit card APRs, especially for good credit.

- Credit Score Impact: Can positively impact your credit score by converting revolving debt to installment debt.

Balance Transfer Credit Cards

These cards allow you to transfer balances from high-interest credit cards to a new card, often with a 0% introductory APR for a promotional period (e.g., 12-21 months). This can be an excellent way to pay down debt rapidly without incurring interest, provided you can pay off the balance before the promotional period ends.

While attractive, it’s crucial to be aware of balance transfer fees, which typically range from 3% to 5% of the transferred amount. If you don’t pay off the balance within the introductory period, the interest rate can jump significantly.

Home Equity Loans or Lines of Credit (HELOCs)

If you own a home, you might consider using your home equity to consolidate debt. Home equity loans provide a lump sum, while HELOCs offer a revolving line of credit. These options typically have lower interest rates because your home serves as collateral, but they also carry the risk of foreclosure if you fail to make payments.

The decision to use home equity for debt consolidation should not be taken lightly. It’s important to understand the associated risks and ensure you have a solid repayment plan in place.

Each consolidation method has its merits and drawbacks. A thorough assessment of your financial situation and careful comparison of terms and conditions are vital to selecting the most effective strategy for your debt reduction goals in 2026.

Calculating Your Potential Savings and Eligibility

Before committing to any consolidation strategy, it’s crucial to calculate your potential savings and assess your eligibility. The goal is to reduce your monthly payments by at least 20%, but the actual savings can vary widely based on your current interest rates, the consolidation option you choose, and your creditworthiness. Understanding these factors will empower you to make an informed decision.

In 2026, various online tools and financial calculators can help you estimate your savings, providing a clearer picture of your financial future. Don’t overlook the importance of these preliminary steps.

Estimating Your Monthly Payment Reduction

To estimate your savings, compare the total of your current minimum credit card payments and interest rates with the projected single monthly payment and interest rate of the consolidation option. For example, if you’re paying $500 monthly across several cards at an average of 20% APR, and a consolidation loan offers a 10% APR with a $400 monthly payment, you’ve achieved a 20% reduction.

Consider the total interest paid over the life of the loan as well, not just the monthly payment. A longer repayment term might offer lower monthly payments but could result in more interest paid overall.

Key Eligibility Factors

Lenders evaluate several criteria when considering consolidation loan applications:

- Credit Score: A higher credit score generally qualifies you for lower interest rates. Lenders often look for scores above 670 for favorable terms.

- Debt-to-Income Ratio (DTI): This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to manage new debt.

- Employment Stability: Lenders prefer applicants with a stable employment history, indicating a reliable income source for repayment.

- Income: Sufficient income to comfortably cover the new consolidated payment is essential.

By understanding and improving these factors, you can significantly increase your chances of securing a consolidation option that truly helps reduce your monthly payments and move towards financial freedom. Preparing your financial documents and understanding your credit report are excellent first steps.

The Application Process and What to Expect

Once you’ve identified the most suitable consolidation option, the next step is the application process. While it might seem daunting, understanding the typical stages and requirements can make it much smoother. The process is designed to allow lenders to assess your financial health and determine the terms they can offer, ultimately aiming to help you achieve your goal of reducing monthly payments.

Preparation is key. Gathering all necessary documents beforehand will expedite the process and prevent unnecessary delays, ensuring a more efficient path to debt relief.

Required Documentation

Lenders will typically request several documents to verify your identity, income, and debt obligations. These may include:

- Proof of identity (e.g., driver’s license, passport)

- Proof of income (e.g., pay stubs, tax returns, bank statements)

- Proof of residence (e.g., utility bill, lease agreement)

- Details of your existing credit card debts (account numbers, balances, interest rates)

Steps in the Application Process

The application process generally follows these steps:

- Research and Compare: As discussed, identify the best consolidation option based on your eligibility and financial goals.

- Pre-qualification (Optional but Recommended): Many lenders offer pre-qualification, which allows you to see potential rates and terms without impacting your credit score.

- Complete the Application: Fill out the official application form, providing accurate and complete information.

- Submit Documentation: Provide all requested supporting documents.

- Lender Review: The lender will review your application and conduct a hard credit inquiry, which may temporarily affect your credit score.

- Receive Offer and Accept: If approved, you’ll receive an offer detailing the loan terms. Review it carefully before accepting.

- Debt Repayment: Once the loan is funded, the money is typically sent directly to your credit card companies to pay off your balances.

Throughout this process, clear communication with your chosen lender is vital. Don’t hesitate to ask questions if any part of the terms or process is unclear. A smooth application process is the first step towards realizing the benefits of credit card debt consolidation in 2026.

Maintaining Financial Discipline Post-Consolidation

Consolidating your credit card debt is a significant step towards financial freedom, but it’s not a magic bullet. The real success lies in maintaining financial discipline afterward. Without a change in spending habits, you risk accumulating new debt, potentially putting you back in a worse position than before. The goal is to not only reduce your monthly payments by 20% but to sustain that improvement and fully eradicate your debt.

This phase is crucial for solidifying your financial health. It requires commitment, careful budgeting, and a proactive approach to managing your money.

Key Strategies for Long-Term Success

- Create and Stick to a Budget: A detailed budget helps you track your income and expenses, identifying areas where you can save and ensuring you have enough to cover your consolidated payment.

- Avoid New Credit Card Debt: This is paramount. Resist the urge to use your newly freed-up credit lines. Consider closing some accounts if temptation is a significant issue.

- Build an Emergency Fund: Having savings set aside for unexpected expenses can prevent you from relying on credit cards in emergencies. Aim for 3-6 months of living expenses.

- Monitor Your Credit Report: Regularly check your credit report for accuracy and to track your progress. A better credit score can open doors to more favorable financial products in the future.

- Continue Financial Education: Stay informed about personal finance best practices. The more you know, the better equipped you are to make sound financial decisions.

Remember, credit card debt consolidation in 2026 is a tool, not a solution in itself. Your commitment to responsible financial behavior is what truly transforms your financial landscape. By adopting these disciplines, you can ensure that your reduced monthly payments translate into long-term financial stability and peace of mind.

Alternative Debt Relief Options Beyond Consolidation

While credit card debt consolidation in 2026 is an effective strategy for many, it’s not the only path to financial relief. For some individuals, especially those with very poor credit or overwhelming debt, alternative options might be more appropriate or necessary. Understanding these alternatives ensures you explore every viable solution to regain control of your finances and reduce your monthly obligations.

It’s important to recognize that different situations call for different approaches. A comprehensive understanding of all available options can guide you to the best decision for your unique circumstances.

Debt Management Plans (DMPs)

Offered by non-profit credit counseling agencies, DMPs involve working with counselors who negotiate with your creditors to lower interest rates and waive fees. You make one monthly payment to the counseling agency, which then distributes the funds to your creditors. These plans typically last 3-5 years.

- Lower Interest Rates: Counselors often secure reduced rates, making debt repayment faster.

- Structured Repayment: Provides a clear path to debt freedom with a single monthly payment.

- Credit Counseling: Offers valuable financial education and budgeting assistance.

Debt Settlement

Debt settlement involves negotiating with creditors to pay a lump sum that is less than the total amount owed. This option is typically pursued when a person is significantly behind on payments or facing severe financial hardship. While it can reduce the amount you owe, it can also severely damage your credit score for several years.

Be wary of debt settlement companies that charge upfront fees or guarantee unrealistic outcomes. Always research and choose reputable agencies.

Bankruptcy

For individuals with insurmountable debt, bankruptcy (Chapter 7 or Chapter 13) may be the last resort. This legal process can discharge certain debts or reorganize them into a manageable payment plan. While it offers a fresh start, bankruptcy has severe and long-lasting negative impacts on your credit score and financial reputation.

Consulting with a qualified bankruptcy attorney is essential to understand the implications and determine if this is the right course of action for your specific situation.

Exploring these alternative debt relief options is crucial if credit card debt consolidation doesn’t seem like the right fit. Each path has its own set of benefits and consequences, and choosing wisely is key to achieving lasting financial recovery.

| Key Aspect | Brief Description |

|---|---|

| Consolidation Goal | Combine multiple debts into one, aiming to reduce monthly payments and interest. |

| Primary Benefit | Lower interest rates and simplified payments, often reducing monthly outlay by 20%+. |

| Common Options | Personal loans, balance transfer cards, home equity loans/HELOCs. |

| Key to Success | Financial discipline, budgeting, and avoiding new debt post-consolidation. |

Frequently Asked Questions About Debt Consolidation in 2026

The primary benefit is simplifying your financial obligations by combining multiple high-interest credit card debts into a single, more manageable payment, often with a lower interest rate, which can significantly reduce your monthly outlay and the total amount paid over time.

You can achieve this by securing a consolidation loan or balance transfer card with a significantly lower interest rate than your current credit cards. The reduced interest means more of your payment goes to the principal, lowering your overall monthly cost and accelerating debt repayment.

While requirements vary, a good to excellent credit score (typically 670 and above) will yield the most favorable interest rates and terms for consolidation loans or balance transfer cards. Lower scores may still qualify but with higher rates.

Yes, risks include potentially longer repayment terms, which can increase total interest paid, or the temptation to accumulate new debt on freed-up credit cards. Using home equity for consolidation also risks losing your home if payments are missed.

Alternatives include debt management plans (DMPs) through credit counseling agencies, debt settlement, or, as a last resort for severe cases, bankruptcy. Each option has different impacts on your finances and credit report, so careful consideration is advised.

Conclusion

Navigating the complexities of credit card debt can be challenging, but solutions like credit card debt consolidation in 2026 offer a tangible pathway to financial relief. By strategically combining your debts into a single, more manageable payment, often with a significantly lower interest rate, you can realistically aim to reduce your monthly payments by 20% or even more. This not only simplifies your financial life but also frees up capital that can be directed towards other financial goals, such as building an emergency fund or investing. However, the true success of consolidation hinges on a commitment to financial discipline post-consolidation. Without a solid budget and a conscious effort to avoid accumulating new debt, even the most effective consolidation strategy may fall short. Explore your options, understand the terms, and embark on a journey toward lasting financial stability.