Senate Bill S.B. 123: Capping Credit Card Late Fees at $25 by 2026

Anúncios

Senate Bill S.B. 123, introduced to cap credit card late fees at $25 starting July 2026, will significantly reshape credit card issuer profitability and consumer financial obligations across the United States.

Anúncios

The recent introduction of Senate Bill S.B. 123 to Cap Credit Card Late Fees at $25 Starting July 2026: Impact on Issuers marks a pivotal moment for both the credit card industry and millions of American consumers. This legislative move aims to curb what many consider excessive fees, potentially reshaping the financial landscape for credit card users and providers alike. How will this change ripple through the economy?

Anúncios

Understanding Senate Bill S.B. 123: The Core Proposal

Senate Bill S.B. 123 represents a significant legislative effort to regulate credit card late fees, a long-standing point of contention for consumers. The core of the proposal is straightforward: cap these fees at a maximum of $25, a substantial reduction from the current average charges that can often exceed $40. This cap is slated to take effect in July 2026, providing a transition period for the industry to adapt.

The impetus behind S.B. 123 stems from a broader push for consumer protection and financial fairness. Proponents argue that current late fees are disproportionately high, often bearing little relation to the actual cost incurred by issuers when a payment is delayed. These fees, they contend, primarily serve as a profit center for banks rather than a genuine deterrent or cost recovery mechanism. The bill seeks to rebalance this dynamic, ensuring that penalties are reasonable and equitable.

Historical context of late fees

To fully grasp the significance of S.B. 123, it’s essential to look at the history of credit card late fees. Historically, these fees were largely unregulated, allowing issuers considerable leeway in setting their charges. Over time, as credit card usage grew, so did the profitability of these fees, leading to increased scrutiny from consumer advocacy groups and lawmakers.

- Early 2000s: Limited regulation, fees often varied widely.

- CARD Act of 2009: Introduced some caps and rules, but allowed for higher fees in certain circumstances, particularly for repeat offenders.

- Current Landscape: Fees can reach up to $41 for subsequent late payments, often criticized as punitive.

The proposed $25 cap is not an arbitrary figure; it aligns with recommendations from consumer protection agencies, which have long advocated for a more reasonable ceiling. This move is expected to have a profound effect on millions of Americans who occasionally miss a payment, potentially saving them billions of dollars annually in unnecessary charges. It also signals a broader shift towards more stringent oversight of financial products and services.

In essence, S.B. 123 is a legislative response to persistent calls for fairness in the credit card market. By establishing a clear and lower ceiling for late fees, the bill aims to alleviate financial burdens on consumers while challenging credit card issuers to reassess their revenue models and operational efficiencies.

Anticipated Impact on Credit Card Issuers

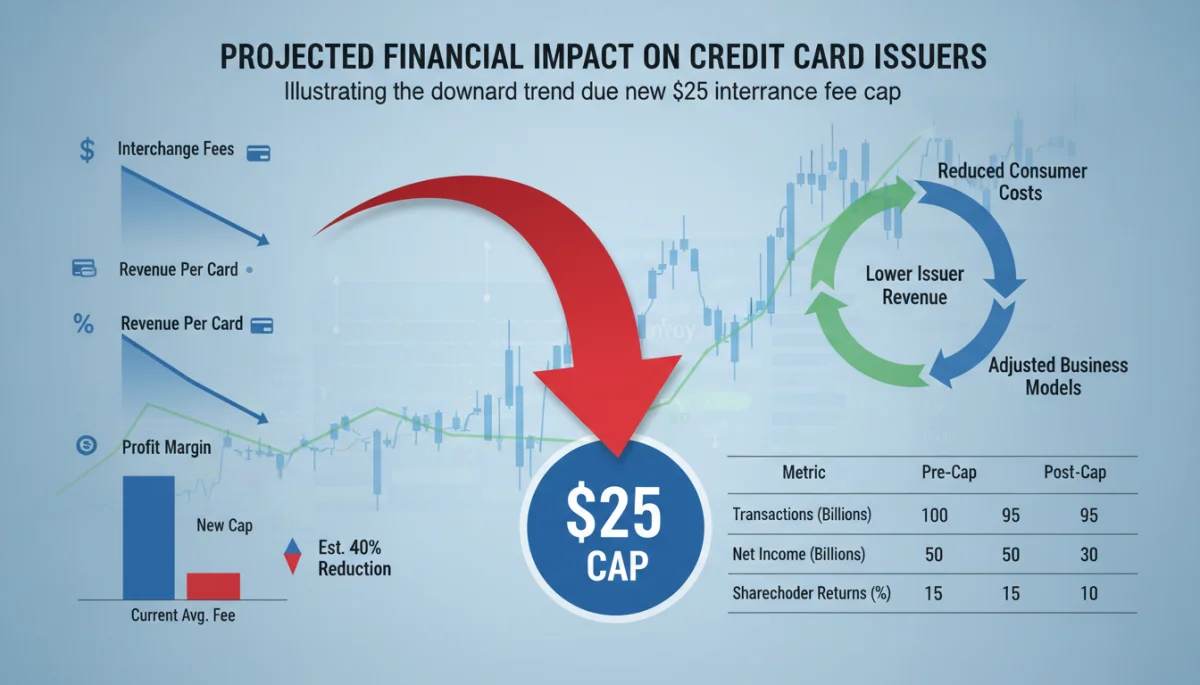

The introduction of Senate Bill S.B. 123 and its proposed cap on credit card late fees at $25 is poised to send significant ripples through the credit card industry. For issuers, late fees constitute a substantial revenue stream, and a reduction of this magnitude will necessitate a comprehensive re-evaluation of their business models and financial projections. The immediate impact will likely be a noticeable decrease in non-interest income, pushing banks to explore alternative strategies to maintain profitability.

Issuers have historically relied on late fees as a dual-purpose tool: a deterrent against missed payments and a significant source of revenue. With the cap, the deterrent effect might diminish for some consumers, though the financial penalty remains. The primary challenge will be compensating for the lost income, which could run into billions of dollars across the industry. This might lead to a period of strategic adjustments and potential innovation in how credit card products are offered and managed.

Potential revenue adjustments and responses

Credit card issuers are not passive entities; they will undoubtedly respond to this legislative change with a range of strategies. These responses could vary from subtle adjustments to more overt changes in their product offerings and fee structures. Understanding these potential shifts is crucial for both consumers and market observers.

- Increased Annual Fees: Some issuers might introduce or increase annual fees on certain card products, especially those that previously relied heavily on late fee revenue from a specific segment of their customer base.

- Higher Interest Rates: There could be a tendency to slightly raise Annual Percentage Rates (APRs) for new accounts or even existing variable-rate accounts, particularly for consumers with lower credit scores who are more prone to late payments.

- Reduced Rewards Programs: Issuers might scale back the generosity of rewards programs, such as cashback percentages, travel points, or sign-up bonuses, to offset lost revenue.

- Stricter Underwriting Standards: Banks might become more selective in their lending practices, tightening credit requirements for new applicants, especially those perceived as higher risk.

- Enhanced Payment Reminders: To proactively reduce late payments, issuers might invest more in automated payment reminders, financial literacy tools, and proactive customer service outreach.

The industry’s response will not be uniform. Larger banks with diverse revenue streams might absorb the impact more easily, while smaller or specialized lenders could face more significant challenges. The competitive landscape will also play a role, as issuers will be wary of making changes that could drive customers to competitors. This period leading up to July 2026 will be critical for strategic planning within these financial institutions.

Ultimately, the impact on issuers will be a test of their adaptability. While the initial reaction might be concern over lost revenue, it could also spur innovation in customer engagement and risk management, potentially leading to a more stable and transparent credit card market in the long run.

Implications for Consumers: What to Expect

For consumers, the proposed cap on credit card late fees at $25 by July 2026 presents a mixed but generally positive outlook. The most immediate and tangible benefit is the potential for significant savings for those who occasionally miss a payment deadline. This direct financial relief could free up disposable income, particularly for individuals living paycheck to paycheck, where a $40+ late fee can represent a considerable burden.

Beyond direct savings, the bill aims to foster a fairer financial environment. Many consumers feel that current late fees are predatory, trapping them in cycles of debt. A lower, more reasonable cap could alleviate some of this psychological and financial pressure, making credit card usage feel less punitive when minor errors occur. It could also encourage more responsible credit management by focusing on principal and interest rather than excessive penalties.

Potential downsides for cardholders

While the benefits are clear, it’s also important for consumers to be aware of potential indirect consequences. As credit card issuers adjust their business models to compensate for lost late fee revenue, these changes could manifest in ways that indirectly affect cardholders.

- Reduced Access to Credit: Banks might become more cautious in extending credit to individuals with lower credit scores or limited credit histories, potentially making it harder for some to obtain credit cards.

- Fewer Promotional Offers: The frequency or attractiveness of balance transfer offers, 0% APR introductory periods, and other promotional deals might decrease as issuers seek to optimize profitability margins.

- Changes in Card Features: Some fringe benefits or less-utilized card features might be scaled back or eliminated to cut costs.

Consumers should actively monitor their credit card statements and terms and conditions as July 2026 approaches and beyond. Understanding these potential shifts will allow them to make informed decisions about their credit usage and choose products that best suit their financial needs. The overall goal of S.B. 123 is to protect consumers, and while some adjustments might occur, the overarching benefit of reduced late fees is expected to outweigh potential drawbacks for the majority.

In summary, while consumers stand to gain directly from lower late fees, they should remain vigilant regarding other potential changes in credit card offerings. The market will adapt, and staying informed will empower consumers to navigate these evolving financial landscapes effectively.

Economic Projections and Market Adjustments

The economic ramifications of Senate Bill S.B. 123 are projected to be multifaceted, influencing not only the credit card industry but also broader consumer spending patterns and financial stability. Analysts are already beginning to model the potential shifts in revenue for issuers and the corresponding impact on consumers’ disposable income. The transition period leading up to July 2026 will be critical for market adjustments, as financial institutions refine their strategies and consumers adapt to the new regulatory environment.

Initial economic projections suggest a significant re-allocation of funds. Billions of dollars that would have gone towards late fees will now remain in consumers’ pockets, potentially stimulating other areas of the economy. This shift could lead to increased consumer spending, savings, or debt repayment, depending on individual financial circumstances. However, the exact magnitude and distribution of this impact will depend on how issuers respond and how consumers alter their financial behaviors.

Industry-wide financial modeling

Financial institutions are currently engaged in complex modeling to understand the full scope of S.B. 123’s impact. This involves assessing historical late fee revenue, forecasting future losses, and strategizing on how to mitigate these impacts. The adjustments will likely be gradual, reflecting the competitive nature of the credit card market.

The market is expected to adapt through a combination of the aforementioned strategies, such as modest increases in APRs for some segments or adjustments to rewards programs. The key will be to find a new equilibrium where profitability is maintained without alienating customers or becoming uncompetitive. This could also spur innovation in areas like personalized financial management tools designed to help consumers avoid late payments altogether.

Furthermore, the long-term economic impact could include a slight reduction in the overall profitability of the credit card sector, potentially leading to consolidation among smaller issuers or a renewed focus on other financial products. However, the industry is resilient, and it’s likely that new revenue streams or efficiencies will emerge to compensate for the changes. The market will ultimately rebalance, but the path to that new balance will be closely watched by regulators and consumers alike.

In essence, S.B. 123 is not just a fee cap; it’s a catalyst for a broader economic recalibration within the credit card ecosystem, with implications stretching far beyond the immediate reduction of late charges.

Regulatory Precedents and Future Outlook

The introduction of Senate Bill S.B. 123 is not an isolated event but rather fits into a broader pattern of increasing regulatory scrutiny over financial services, particularly those impacting consumers. Understanding the regulatory precedents provides context for S.B. 123 and offers insights into the future direction of consumer finance legislation. The CARD Act of 2009, for instance, established foundational protections for credit card users, and S.B. 123 can be seen as an evolution of these efforts, building on past successes and addressing areas where further protection is deemed necessary.

This legislative trend reflects a growing emphasis on fairness, transparency, and consumer empowerment within the financial sector. Regulators are increasingly focused on curbing practices perceived as exploitative or unduly burdensome, signaling a shift towards a more consumer-centric financial landscape. The future outlook suggests continued vigilance and potential for further legislative action in areas like overdraft fees, interchange fees, or even the structure of interest rates.

Broader regulatory landscape

The regulatory environment is dynamic, constantly evolving in response to market conditions, technological advancements, and public sentiment. S.B. 123 could very well serve as a precedent for similar actions in other financial product categories.

- Overdraft Fees: There’s ongoing discussion and regulatory pressure to reduce or eliminate excessive overdraft fees charged by banks.

- Interchange Fees: Merchant groups frequently advocate for lower interchange fees, which are paid by merchants to card-issuing banks for processing transactions.

- Data Privacy: Growing concerns over financial data privacy and security are likely to lead to more stringent regulations for how financial institutions collect, store, and use consumer data.

The political climate also plays a significant role in shaping financial regulation. Administrations and legislative bodies with a strong consumer protection agenda are more likely to pursue bills like S.B. 123. As such, the outcome of future elections and the composition of legislative bodies will be key indicators of the future regulatory outlook for the financial industry.

The long-term impact of S.B. 123 extends beyond just late fees; it reinforces the principle that financial institutions have a responsibility to operate fairly and transparently. This could lead to a more ethical and sustainable financial system, benefiting consumers and fostering greater trust in financial services. The future of credit card regulation appears to be heading towards greater consumer advocacy and protection.

Strategic Adaptations for Credit Card Issuers

With the looming July 2026 deadline for the credit card late fees cap, credit card issuers are already engaging in strategic planning to adapt to the new regulatory environment. This isn’t merely about cutting costs; it’s about fundamentally rethinking how they generate revenue, manage risk, and interact with their customer base. Those who adapt effectively will maintain their market position, while those who fail to innovate may see their profitability erode.

One primary area of adaptation will be in refining their risk assessment models. If late fees become less lucrative, issuers might need more sophisticated ways to identify and manage customers who are prone to late payments. This could involve leveraging advanced analytics and artificial intelligence to predict payment behavior more accurately, allowing for proactive interventions rather than punitive fees.

Innovation in product offerings

To offset the loss of late fee revenue, issuers will likely focus on innovating their product offerings to attract and retain customers through value-added services rather than fee-based income. This could manifest in several ways:

- Premium Services: Developing and marketing premium card products with higher annual fees but exclusive benefits, such as enhanced travel insurance, concierge services, or luxury perks.

- Financial Wellness Tools: Integrating more robust financial management tools, budgeting apps, and credit-building resources directly into their platforms to help customers avoid late payments and improve financial health.

- Subscription Models: Exploring subscription-based services for certain card features or benefits, offering a predictable revenue stream outside of traditional fees.

- Personalized Offers: Using data to create highly personalized credit card offers and rewards programs that cater to individual spending habits and preferences, fostering greater customer loyalty.

Furthermore, there will be an increased emphasis on operational efficiency. Streamlining internal processes, reducing overhead, and optimizing customer service interactions can all contribute to maintaining profitability in a lower-fee environment. The goal is to create a more robust and sustainable business model that is less reliant on penalty-driven income.

Ultimately, S.B. 123 presents both a challenge and an opportunity for credit card issuers. It forces them to innovate and focus more on core value propositions and customer relationships, potentially leading to a more competitive and consumer-friendly market in the long run.

Navigating the Future of Credit Card Finance

The impending cap on credit card late fees ushered in by Senate Bill S.B. 123 beginning in July 2026 marks a significant milestone in the evolution of credit card finance in the United States. This legislative change is not merely a tweak to a single fee; it represents a philosophical shift towards greater consumer protection and a challenge to the traditional revenue models of credit card issuers. Navigating this future will require adaptability from financial institutions and increased awareness from consumers.

For financial institutions, the next few years will be a period of intense strategic recalibration. They will need to innovate their product offerings, optimize their operational efficiencies, and re-evaluate their risk management practices. The focus will likely shift from relying on penalty fees to fostering stronger, more value-driven relationships with their cardholders. This could lead to a more competitive market where card features, rewards, and customer service become even more critical differentiators.

Consumer preparedness and advocacy

On the consumer side, preparedness is key. While the $25 cap on late fees offers direct financial relief, consumers should remain vigilant and informed about how issuers might adjust other aspects of their credit card programs. This includes:

- Reviewing Terms and Conditions: Regularly checking for updates to interest rates, annual fees, and rewards programs.

- Monitoring Credit Scores: Understanding how changes in lending standards might affect access to credit.

- Utilizing Financial Tools: Taking advantage of budgeting apps, payment reminders, and financial literacy resources to avoid late payments altogether.

- Engaging with Advocacy Groups: Supporting organizations that champion consumer financial protection to ensure a continued focus on fair practices.

The journey towards a more equitable credit card landscape is ongoing. S.B. 123 is a powerful step in that direction, but it is unlikely to be the last. Both industry and consumers will need to remain engaged and adaptable as the financial ecosystem continues to evolve. The ultimate goal is a credit card market that serves as a beneficial financial tool for all, rather than a source of unexpected penalties.

In essence, the future of credit card finance, shaped by bills like S.B. 123, promises a landscape where consumer welfare plays a more central role, encouraging greater transparency and fairness across the board.

| Key Aspect | Description |

|---|---|

| Bill S.B. 123 Core | Caps credit card late fees at $25 starting July 2026. |

| Impact on Issuers | Significant revenue loss, leading to business model adjustments, potential fee changes. |

| Impact on Consumers | Direct savings on late fees, but potential for other fee increases or stricter credit access. |

| Future Outlook | A shift towards more consumer-centric financial regulation and industry innovation. |

Frequently Asked Questions About S.B. 123

The primary goal of Senate Bill S.B. 123 is to cap credit card late fees at a maximum of $25. This aims to protect consumers from excessive charges and foster a fairer financial environment by reducing the financial burden associated with missed payments.

The provisions of Senate Bill S.B. 123, including the $25 cap on credit card late fees, are scheduled to take effect starting in July 2026. This provides a transition period for credit card issuers to adjust their business models and operational strategies accordingly.

Issuers may respond by adjusting other fees, such as annual fees or interest rates, or by altering rewards programs. They might also tighten underwriting standards and enhance payment reminder services to mitigate the impact of lost late fee revenue.

While the bill applies broadly, its impact might vary across different card types and issuers. Premium cards with higher annual fees may see less direct impact on their overall profitability, while cards targeting subprime borrowers might experience more significant changes in their offerings.

Consumers should monitor their credit card terms, review statements for any changes, and focus on timely payments to avoid all fees. Staying informed about credit card offerings and utilizing financial management tools will be crucial to navigating the evolving landscape.

Conclusion

Senate Bill S.B. 123, with its mandate to cap credit card late fees at $25 from July 2026, undeniably marks a transformative moment for the credit card industry and its consumers. This legislative intervention underscores a broader commitment to consumer protection, aiming to mitigate the financial strain often imposed by exorbitant penalty fees. While credit card issuers face the challenge of adapting their revenue models, potentially through adjustments to other fees or product offerings, consumers stand to benefit from more predictable and fairer charges.

The path forward will necessitate strategic innovation from financial institutions, pushing them towards more value-driven services and enhanced customer engagement. For consumers, the onus will be on vigilance and informed decision-making, ensuring they understand the evolving terms of their credit products. Ultimately, S.B. 123 is poised to reshape the financial landscape, fostering a credit card environment that is both more equitable and sustainable for all stakeholders.