US Credit Card Debt Hits $6,500 in Q1 2026: Expert Analysis

Anúncios

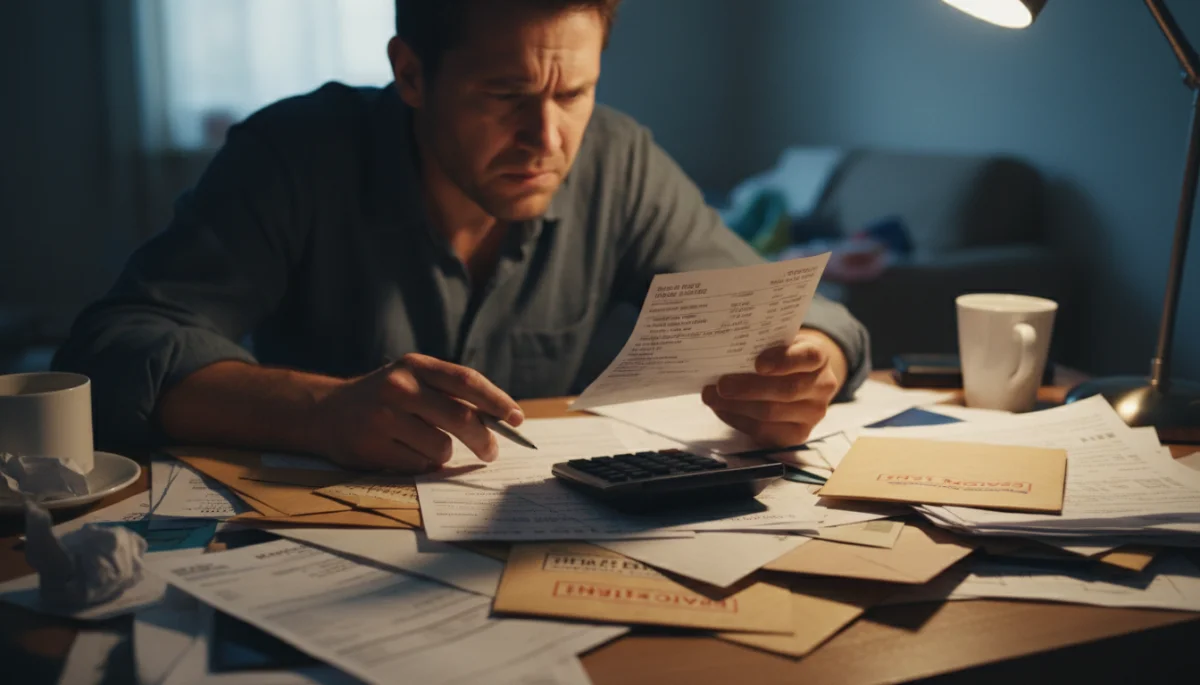

The first quarter of 2026 saw average American credit card debt climb to $6,500, a figure prompting significant expert analysis on underlying economic trends and consumer financial health.

Anúncios

The latest financial reports have sent ripples through the American economy, revealing a significant milestone: the average American credit card debt has reached an unprecedented $6,500 in Q1 2026. This figure isn’t just a number; it’s a critical indicator of shifting economic trends and consumer behavior across the United States. What factors are driving this increase, and what does it signal for the future of personal finance?

Anúncios

Understanding the Q1 2026 Credit Card Debt Surge

The recent data indicating that average American credit card debt has climbed to $6,500 in the first quarter of 2026 demands immediate attention. This surge is not an isolated event but rather a symptom of broader economic forces at play, affecting millions of households across the nation. Unpacking this trend requires a look into both macro and microeconomic factors that contribute to consumer borrowing habits.

Several key elements are believed to be fueling this increase. Inflation, while showing signs of moderation, has persistently eroded purchasing power, pushing consumers to rely more heavily on credit for everyday expenses. Additionally, interest rates on credit cards have remained elevated, making it more challenging for individuals to pay down their balances, leading to an accumulation of debt over time.

Inflationary Pressures and Consumer Spending

The persistent inflationary environment has been a significant contributor to the rise in credit card debt. As the cost of living continues to climb, many Americans find their paychecks stretching less than before. This forces a reliance on credit to cover essential expenditures.

- Higher costs for groceries and utilities.

- Increased housing and transportation expenses.

- Stagnant wage growth for many households.

These factors collectively reduce discretionary income and push families towards credit lines to bridge financial gaps.

Impact of Elevated Interest Rates

The Federal Reserve’s efforts to combat inflation through interest rate hikes have had a direct impact on credit card holders. Higher benchmark rates translate to higher Annual Percentage Rates (APRs) on credit cards, making carrying a balance significantly more expensive.

This dynamic creates a vicious cycle where consumers struggle to make meaningful progress on their principal debt, as a larger portion of their monthly payments goes towards interest. The longer the balance remains, the more interest accrues, contributing to the overall debt burden.

In conclusion, the $6,500 average credit card debt in Q1 2026 is a complex issue rooted in a combination of persistent inflation and high interest rates. These economic conditions are compelling consumers to lean on credit more heavily, making debt reduction a significant challenge for many.

Economic Trends Driving Increased Borrowing

The current economic landscape in Q1 2026 presents a multifaceted picture, where various trends converge to influence consumer borrowing. Beyond inflation and interest rates, other significant factors are at play, shaping how Americans manage their finances and their propensity to incur credit card debt. Understanding these broader trends is crucial for a comprehensive analysis of the current debt situation.

One notable trend is the continued expansion of access to credit, with many lenders offering more attractive introductory rates or rewards programs. While seemingly beneficial, these offers can sometimes encourage overspending, particularly among individuals who may not fully grasp the long-term implications of carrying high balances. Furthermore, shifts in employment patterns and income stability also contribute to the overall economic environment impacting debt levels.

Labor Market Dynamics and Income Volatility

The labor market, while generally robust, exhibits pockets of instability, particularly in certain sectors. Job displacement due to automation or economic restructuring can lead to periods of unemployment or underemployment, forcing individuals to rely on credit cards to cover living expenses.

- Sector-specific job losses affecting income.

- Rise of the gig economy with less stable income streams.

- Delayed wage increases failing to keep up with cost of living.

These factors contribute to income volatility, making financial planning more challenging and increasing the likelihood of resorting to credit.

Consumer Confidence and Spending Habits

Consumer confidence plays a pivotal role in spending patterns. Despite economic headwinds, a certain level of optimism, or perhaps a sense of urgency to acquire goods before further price increases, can drive spending. This often translates into increased credit card usage for both necessities and discretionary purchases.

The psychological aspect of using credit, where the immediate impact of spending is delayed, also contributes to higher debt. Consumers might feel less constrained when swiping a card compared to using cash, leading to a gradual accumulation of debt without immediate awareness.

The economic trends driving increased borrowing are a complex interplay of market forces, employment stability, and consumer psychology. These elements collectively explain why many Americans are finding themselves increasingly reliant on credit cards, pushing the average debt higher.

Impact on Household Budgets and Financial Stability

The rise in average American credit card debt to $6,500 in Q1 2026 has direct and significant implications for household budgets and overall financial stability across the nation. This elevated debt level is not merely an abstract economic statistic; it translates into real-world challenges for families trying to manage their daily finances, save for the future, and achieve long-term financial security. Understanding these impacts is crucial for grasping the gravity of the current situation.

For many households, higher credit card balances mean a larger portion of their income is allocated to debt servicing—making minimum payments that primarily cover interest rather than principal. This reduces the funds available for other essential expenses, savings, or investments. The ripple effect can be felt in various aspects of family life, from delaying major purchases to impacting mental well-being due to financial stress.

Reduced Disposable Income

When credit card payments consume a larger share of monthly income, families have less money left for other expenditures. This directly impacts their ability to save, invest, or even afford unexpected emergencies.

- Less money for discretionary spending.

- Difficulty building emergency savings.

- Struggles to meet other financial obligations.

This reduction in disposable income can create a cycle of dependency on credit, further exacerbating the debt problem.

Increased Financial Stress and Mental Health

The constant pressure of managing high credit card debt can take a significant toll on an individual’s and a family’s mental and emotional health. Financial stress is a pervasive issue that can lead to anxiety, depression, and relationship problems.

The feeling of being trapped in a cycle of debt, with seemingly no way out, can be overwhelming. This stress can impact productivity at work, overall well-being, and even physical health, creating a holistic challenge for those affected. Addressing the debt isn’t just about financial numbers; it’s about restoring peace of mind.

In summary, the increased credit card debt significantly strains household budgets, leading to reduced financial flexibility and heightened stress. These consequences underscore the importance of proactive financial management and support for individuals struggling with debt.

Expert Analysis: What the Data Reveals for Q1 2026

Financial experts across the nation are meticulously dissecting the Q1 2026 report, which highlights the average American credit card debt reaching $6,500. Their analyses go beyond the headlines, seeking to uncover the nuanced factors and potential long-term implications of this trend. These insights are invaluable for policymakers, financial institutions, and individual consumers alike, providing a clearer picture of the economic forces at play.

Many economists point to a combination of persistent inflation, which has outpaced wage growth for a significant portion of the population, and the lagged effect of rising interest rates. While the Federal Reserve has been aggressive in its monetary policy to curb inflation, the impact on consumer debt is often felt with a delay, as existing balances roll over at higher APRs and new borrowing becomes more costly. Analysts are also examining consumer behavior, looking for shifts in spending priorities and financial literacy.

Forecasting Future Debt Trajectories

Experts are divided on the immediate future of credit card debt. Some predict a continued upward trajectory if inflationary pressures persist and interest rates remain high, pushing more consumers into reliance on credit. Others believe that as the economy adjusts, there might be a plateau or even a slight decline, especially if households become more conservative with their spending.

- Projections of continued debt growth if economic conditions don’t improve.

- Potential for stabilization as consumers adapt.

- Risk of defaults increasing if debt becomes unmanageable.

The key variable is the interplay between inflation, interest rates, and employment stability, which will dictate consumer borrowing capacity and willingness.

Recommendations for Policy Makers and Consumers

Analysts are also offering guidance. For policymakers, the focus is on strategies to stabilize the economy, manage inflation, and potentially introduce programs that assist consumers with debt relief or financial education. For individuals, the advice centers on prudent financial management, emphasizing budgeting, debt consolidation, and prioritizing high-interest debt repayment.

This includes seeking professional financial advice, exploring debt management plans, and making conscious efforts to reduce reliance on credit for everyday expenses. The goal is to empower consumers to navigate these challenging financial waters more effectively.

Ultimately, expert analysis suggests that the $6,500 average debt is a warning sign. It necessitates a multi-pronged approach involving both systemic economic adjustments and individual financial discipline to mitigate potential long-term adverse effects.

Strategies for Managing and Reducing Credit Card Debt

With the average American credit card debt reaching $6,500 in Q1 2026, it’s more critical than ever for individuals to adopt effective strategies for managing and reducing their debt. While external economic factors play a role, proactive personal financial management can significantly impact one’s ability to navigate these challenging times. There are several proven methods and approaches that can help consumers regain control of their finances and work towards a debt-free future.

The first step often involves a clear understanding of one’s financial situation, including total debt, interest rates on various cards, and monthly income versus expenses. This comprehensive view allows for the creation of a realistic budget and a targeted debt repayment plan. Without a clear picture, efforts to reduce debt can be haphazard and less effective, leading to frustration and continued financial strain.

Budgeting and Expense Tracking

A fundamental strategy for debt reduction is to create and stick to a detailed budget. This involves tracking all income and expenses to identify areas where spending can be cut. By reducing unnecessary expenditures, more funds can be allocated towards debt payments.

- Identify essential versus non-essential spending.

- Cut back on discretionary purchases like dining out or entertainment.

- Automate savings and debt payments to ensure consistency.

Effective budgeting provides a roadmap for financial discipline and helps prevent further debt accumulation.

Debt Repayment Methods: Snowball vs. Avalanche

When it comes to actively paying down debt, two popular methods are the debt snowball and the debt avalanche. The debt snowball method involves paying off the smallest debt first to gain psychological momentum, while the debt avalanche method prioritizes debts with the highest interest rates to save money on interest charges.

Choosing the right method depends on individual preferences and financial psychology. The snowball method provides quick wins, which can be motivating. The avalanche method, though potentially slower to show initial results, is mathematically more efficient, saving more money in the long run. Both require consistent application and commitment.

Implementing effective strategies for managing and reducing credit card debt is essential. Whether through meticulous budgeting or strategic repayment plans, taking proactive steps can empower individuals to overcome financial challenges and improve their economic outlook.

Preventing Future Credit Card Debt Accumulation

Avoiding the pitfalls of accumulating credit card debt, especially in an economic climate where the average American credit card debt has hit $6,500 in Q1 2026, requires foresight and disciplined financial habits. Proactive measures are far more effective than reactive ones when it comes to personal finance. Building a robust financial foundation can shield individuals from future economic shocks and reduce the reliance on high-interest credit.

Key to prevention is developing a strong understanding of personal financial principles and making informed decisions about credit usage. This involves not just managing current debt but also establishing habits that promote long-term financial health. Educating oneself on the true cost of credit and exploring alternatives to borrowing can make a significant difference in preventing future debt accumulation.

Building an Emergency Fund

One of the most effective ways to prevent future credit card debt is to establish a robust emergency fund. This fund acts as a financial safety net, providing resources for unexpected expenses without having to resort to credit cards.

- Aim for 3-6 months of living expenses in savings.

- Automate contributions to the emergency fund.

- Keep the fund separate from regular checking accounts to avoid temptation.

An emergency fund offers peace of mind and protection against unforeseen financial challenges.

Responsible Credit Card Usage

Learning to use credit cards responsibly is paramount. This means understanding credit limits, payment cycles, and the implications of carrying a balance. It also involves being mindful of one’s spending habits and avoiding the temptation to overspend.

Using credit cards primarily for purchases that can be paid off in full each month is an ideal approach. This allows individuals to benefit from rewards and build a positive credit history without incurring interest charges. Regularly reviewing statements and monitoring credit scores are also crucial components of responsible usage.

Preventing future credit card debt involves a combination of strategic savings, disciplined spending, and a deep understanding of how credit works. By taking these proactive steps, individuals can safeguard their financial future and avoid the burden of excessive debt.

The Broader Economic Implications of Rising Debt

The significant increase in average American credit card debt to $6,500 in Q1 2026 extends beyond individual households, carrying substantial broader economic implications. This trend can affect national economic growth, consumer spending patterns, and even the stability of the financial sector. Understanding these wider impacts is crucial for grasping the full scope of the current debt situation in the United States.

High levels of consumer debt can act as a drag on economic growth. When a large portion of consumer income is diverted to debt payments, there is less money available for new purchases, investments, or discretionary spending, which are vital components of a healthy economy. This can lead to a slowdown in retail sales, reduced demand for goods and services, and ultimately, a weaker overall economic performance. The interconnectedness of consumer finance with the broader economy means that individual debt challenges can quickly become systemic issues.

Potential for Economic Slowdown

Rising consumer debt can signal an impending economic slowdown. As more households struggle with debt, their capacity to spend on non-essential items diminishes, impacting various industries.

- Reduced consumer demand for goods and services.

- Negative impact on retail and hospitality sectors.

- Slower overall GDP growth due to decreased consumption.

This creates a feedback loop where economic contraction can further exacerbate debt problems.

Risk to Financial Institutions

While credit card debt is spread across millions of consumers, a widespread inability to repay these debts could pose a risk to financial institutions. Increased defaults could lead to losses for banks and credit card companies, potentially tightening lending standards and impacting the broader financial system.

This scenario, while not immediately imminent, is a concern for regulators and financial analysts. It underscores the importance of monitoring debt levels and ensuring that financial institutions maintain adequate reserves to absorb potential losses. The health of the consumer is intricately linked to the health of the financial system.

In conclusion, the rising average American credit card debt has far-reaching economic implications, potentially leading to slower growth and posing risks to financial stability. Addressing this trend requires a holistic approach that considers both individual financial well-being and broader economic policy.

| Key Point | Brief Description |

|---|---|

| Debt Milestone Q1 2026 | Average American credit card debt reached $6,500, marking a significant increase. |

| Driving Factors | Inflationary pressures, high interest rates, and income volatility are key contributors. |

| Household Impact | Reduced disposable income, increased financial stress, and hindered savings. |

| Prevention & Management | Budgeting, emergency funds, and responsible credit use are crucial strategies. |

Frequently Asked Questions About Credit Card Debt in 2026

The rise is primarily attributed to persistent inflation eroding purchasing power, coupled with elevated interest rates making it harder to pay down balances. Income volatility and increased consumer reliance on credit for daily expenses also contribute significantly to this trend.

Higher credit card debt means a larger portion of income goes towards minimum payments, often covering mostly interest. This reduces disposable income, hindering savings, investments, and leading to increased financial stress for many American families.

Beyond inflation and interest rates, labor market dynamics, such as income volatility in the gig economy, and consumer confidence influencing spending habits are significant drivers. Easy access to credit with attractive initial offers also plays a role.

Effective strategies include meticulous budgeting and expense tracking to identify savings, and employing debt repayment methods like the debt snowball or avalanche. Consolidating high-interest debts and seeking financial counseling are also beneficial approaches.

The rising debt can lead to a general economic slowdown as consumers reduce spending, impacting retail and other sectors. It also poses a potential risk to the financial stability of institutions if widespread defaults were to occur, tightening credit markets.

Conclusion

The report indicating that the average American credit card debt has reached $6,500 in Q1 2026 is a significant economic marker, reflecting a complex interplay of inflation, interest rates, and evolving consumer behaviors. This trend necessitates a dual approach: individuals must embrace disciplined financial management and proactive debt reduction strategies, while policymakers consider broader economic interventions to foster stability. As the nation navigates these financial currents, understanding the causes and consequences of rising debt will be paramount for both personal and national economic health, ensuring a more resilient financial future for all Americans.