2026 Housing Affordability Crisis: First-Time Buyer Strategies

Anúncios

The 2026 housing affordability crisis, characterized by a projected 7% price hike, demands proactive strategies for first-time buyers to navigate market challenges and secure homeownership.

Anúncios

The dream of homeownership remains a cornerstone of the American ideal, yet for many first-time buyers, it feels increasingly out of reach. As we approach 2026, forecasts suggest a significant housing affordability crisis, with a projected 7% price hike further complicating an already challenging market. This isn’t just a statistical blip; it’s a fundamental shift impacting millions of aspiring homeowners. Understanding the forces at play and adopting strategic approaches will be crucial for navigating this complex landscape. This article aims to equip you with the knowledge and actionable steps needed to confront these challenges head-on and make your homeownership dreams a reality.

Anúncios

Understanding the 2026 Housing Market Dynamics

The housing market in 2026 is poised to present a unique set of challenges, particularly for those looking to purchase their first home. Several converging factors are contributing to this projected 7% price hike and the broader affordability crisis. It’s not merely about inflation; it’s a confluence of supply-demand imbalances, evolving economic policies, and demographic shifts that create a perfect storm for aspiring homeowners.

One of the primary drivers is the persistent shortage of housing inventory. Construction rates have struggled to keep pace with population growth and household formation for years, leading to a structural deficit of available homes. This scarcity naturally pushes prices upward as buyers compete for limited properties. Furthermore, rising interest rates, while designed to curb inflation, simultaneously increase the cost of borrowing, making mortgages more expensive and reducing purchasing power for many.

Key Factors Driving Price Increases

Several underlying economic and social trends are exacerbating the housing affordability issue. These factors are deeply interconnected, creating a ripple effect across the entire real estate ecosystem.

- Limited Housing Supply: A chronic undersupply of new homes, coupled with a preference for existing homeowners to retain their properties, restricts available inventory.

- Inflationary Pressures: Increased costs for labor, materials, and land drive up construction expenses, which are then passed on to buyers.

- Demographic Shifts: A large cohort of millennials and Gen Z are entering prime home-buying years, intensifying demand in an already tight market.

- Investment Activity: Institutional investors and cash buyers can often outcompete first-time buyers, further reducing accessible inventory.

Understanding these dynamics is the first step toward formulating effective strategies. The market isn’t just reacting to immediate events; it’s shaped by long-term trends that require a nuanced approach from those hoping to enter it. Acknowledging these challenges early allows for more realistic planning and goal setting.

Financial Preparedness: Building a Strong Foundation

In a market characterized by a 7% price hike, financial preparedness is not just important; it’s paramount. First-time buyers must meticulously assess their financial health and lay a robust foundation to withstand the pressures of a competitive and expensive housing market. This involves more than just saving for a down payment; it encompasses a holistic approach to personal finance, including credit management, debt reduction, and strategic savings.

Starting early is key. The sooner you begin to optimize your finances, the better positioned you will be when it’s time to make an offer. This proactive stance can make a significant difference in securing favorable loan terms and ultimately, in making homeownership a sustainable reality rather than a fleeting aspiration.

Essential Steps for Financial Optimization

Before even looking at properties, dedicate time to strengthening your financial position. This groundwork will pay dividends when navigating the complexities of mortgages and closing costs.

- Credit Score Improvement: A higher credit score can unlock lower interest rates, saving you tens of thousands over the life of a loan. Pay bills on time, reduce credit utilization, and review your credit report for errors.

- Debt-to-Income Ratio Reduction: Lenders scrutinize your DTI. Pay down high-interest debts, such as credit cards and personal loans, to improve this ratio.

- Aggressive Savings for Down Payment: Aim for at least 20% down to avoid Private Mortgage Insurance (PMI), if possible. Explore high-yield savings accounts or investment vehicles that align with your timeline.

- Emergency Fund Creation: Beyond the down payment, ensure you have an emergency fund covering 3-6 months of living expenses. Homeownership comes with unexpected costs.

By focusing on these areas, first-time buyers can significantly enhance their attractiveness to lenders and improve their ability to absorb the higher costs associated with the 2026 housing market. A strong financial footing provides both confidence and leverage in negotiations.

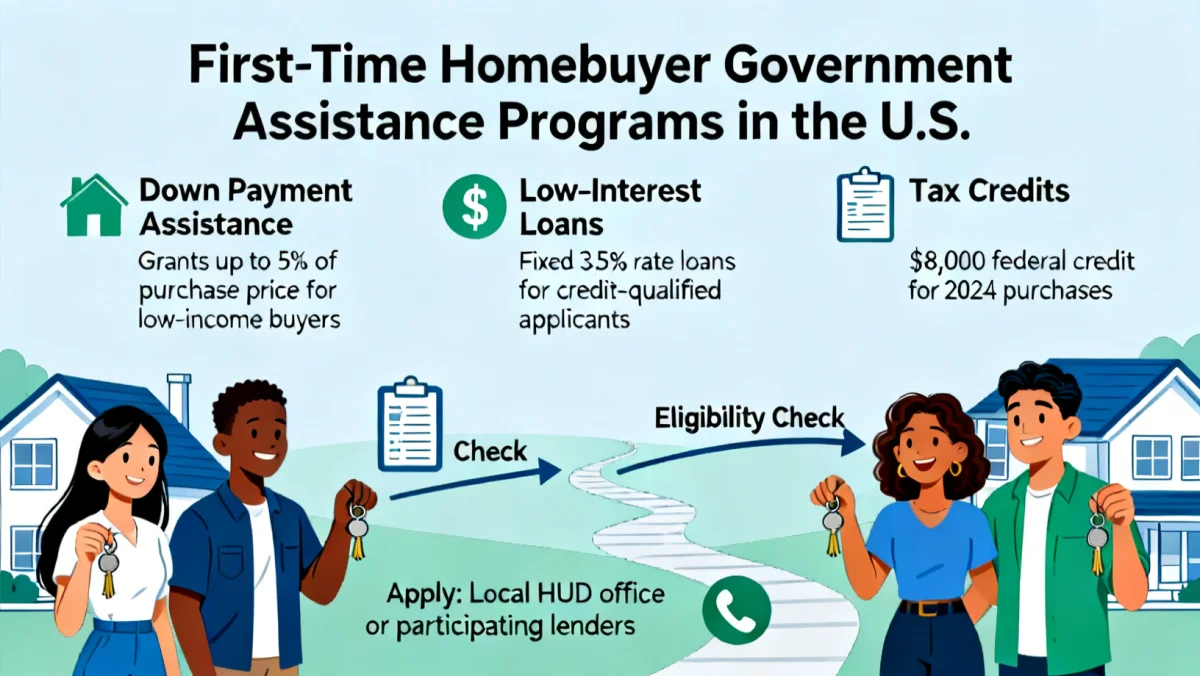

Exploring Government Programs and Assistance

Amidst the projected 7% price hike, first-time buyers often overlook a crucial resource: government programs and assistance. Various federal, state, and local initiatives are specifically designed to help individuals overcome financial hurdles associated with homeownership. These programs can provide significant relief, from down payment assistance to reduced interest rates, making the dream of owning a home more attainable.

It’s important to research what’s available in your specific area, as eligibility requirements and program benefits can vary widely. Don’t assume you don’t qualify; many programs have flexible criteria aimed at supporting a broad range of income levels and demographics. Engaging with a knowledgeable lender or housing counselor can help uncover these opportunities.

Types of Assistance Available

These programs can be a game-changer for first-time buyers struggling to meet the upfront costs of home purchase.

- Down Payment Assistance (DPA): Many programs offer grants or deferred loans to cover a portion or all of your down payment, significantly reducing the initial cash required.

- Low-Interest Rate Loans: Federal Housing Administration (FHA) loans, VA loans (for veterans), and USDA loans (for rural areas) offer more lenient qualification criteria and competitive interest rates.

- First-Time Homebuyer Tax Credits: Some states and localities offer tax credits that can lower your tax burden, effectively putting money back in your pocket.

- Homebuyer Education Programs: These often mandatory courses provide valuable knowledge about the home-buying process, budgeting, and home maintenance, sometimes unlocking access to specific aid.

Leveraging these programs can bridge the gap between aspirational homeownership and actual homeownership, especially when facing a challenging market. They represent a tangible support system for those who might otherwise be priced out.

Strategic Property Search and Negotiation Tactics

When facing a 7% price hike in the 2026 housing market, first-time buyers need to be exceptionally strategic in their property search and negotiation tactics. The traditional approach of simply finding a desirable home and making an offer may no longer suffice. It requires a more nuanced understanding of market trends, a willingness to compromise, and sharp negotiation skills to secure a home at a reasonable price.

This means thinking outside the box, being flexible with your criteria, and preparing for potentially competitive bidding wars. A well-informed and agile approach can make all the difference in a seller’s market where every advantage counts.

Smart Searching and Bidding Strategies

To succeed in a tight market, consider these proactive measures:

- Expand Your Search Radius: Look beyond your ideal neighborhood to areas with slightly lower prices or promising growth potential. Commute times or school districts might need re-evaluation.

- Consider ‘Fixer-Uppers’: Properties requiring minor renovations often come at a lower price point, allowing you to build equity over time. Be realistic about renovation costs and your DIY capabilities.

- Get Pre-Approved, Not Just Pre-Qualified: A full pre-approval demonstrates your financial readiness to sellers, making your offer more appealing.

- Craft a Strong Offer: Beyond the price, consider offering a flexible closing date, waiving certain contingencies (with caution), or writing a personal letter to the seller.

- Work with an Experienced Agent: A local real estate agent with a deep understanding of the 2026 market can provide invaluable insights into pricing, negotiation, and off-market opportunities.

By adopting these strategic approaches, first-time buyers can increase their chances of finding a suitable home and navigating the negotiation process successfully, even in a market with escalating prices.

Long-Term Planning: Sustain Homeownership

Securing a home in the face of a 7% price hike is only half the battle; sustaining homeownership for the long term requires careful planning and financial discipline. Many first-time buyers focus intensely on the purchase itself, sometimes overlooking the ongoing costs and responsibilities that come with owning a property. From property taxes and insurance to maintenance and potential repairs, these expenses can significantly impact your budget.

A proactive approach to long-term financial health ensures that your home remains an asset rather than a burden. This involves continuous budgeting, building a robust home maintenance fund, and understanding the future implications of your mortgage.

Managing Ongoing Homeownership Costs

To maintain financial stability as a homeowner, consider these essential long-term strategies:

- Create a Detailed Home Budget: Include not only mortgage payments but also property taxes, homeowner’s insurance, utilities, and a dedicated fund for repairs and maintenance.

- Build a Home Maintenance Fund: Aim to save 1-3% of your home’s value annually for unexpected repairs and routine upkeep. This prevents costly surprises from derailing your finances.

- Understand Property Tax Increases: Property taxes can rise over time. Research historical trends in your area and factor potential increases into your long-term budget.

- Review Insurance Policies Annually: Ensure your homeowner’s insurance adequately covers your property’s value and potential risks, and shop around for competitive rates.

- Consider Refinancing Opportunities: If interest rates drop in the future, refinancing could lower your monthly payments, freeing up funds for other financial goals.

By establishing these financial habits early, first-time buyers can ensure their homeownership journey is not just successful in the short term but also sustainable and rewarding for years to come.

Alternative Paths to Homeownership

Given the challenges posed by the 2026 housing affordability crisis and the projected 7% price hike, traditional homeownership paths might not be feasible for everyone. Exploring alternative routes can open up new opportunities for first-time buyers to achieve their dream, albeit through unconventional means. These alternatives often require flexibility, patience, and a willingness to consider different property types or ownership structures.

It’s about adapting to the market, not letting the market dictate your aspirations. By broadening your perspective, you might discover innovative ways to enter the real estate ladder that align better with your current financial situation.

Innovative Approaches to Secure a Home

Consider these less traditional, but increasingly relevant, pathways:

- Co-Buying with Friends or Family: Pooling resources with trusted individuals can significantly boost purchasing power, allowing access to more expensive properties or better neighborhoods. Ensure a clear legal agreement is in place.

- Tiny Homes or Modular Housing: These options offer a more affordable entry point into homeownership, often with lower maintenance costs and a smaller environmental footprint. Zoning regulations are a key consideration.

- House Hacking: Purchasing a multi-unit property (duplex, triplex) and living in one unit while renting out the others can help offset mortgage costs, making homeownership more affordable.

- Rent-to-Own Programs: These agreements allow you to rent a property with an option to buy it later, often at a pre-determined price. A portion of your rent may go towards a down payment.

- Community Land Trusts (CLTs): CLTs aim to keep housing permanently affordable by separating land ownership from home ownership, significantly reducing the purchase price of the house itself.

These alternative strategies demonstrate that homeownership isn’t a one-size-fits-all journey. For first-time buyers facing a tough market, these creative solutions can provide a viable path forward, offering flexibility and financial relief.

| Key Strategy | Brief Description |

|---|---|

| Financial Preparedness | Improve credit, reduce debt, and save aggressively for a down payment to strengthen your buying power. |

| Government Assistance | Explore federal, state, and local programs offering down payment aid, low-interest loans, and tax credits. |

| Strategic Search | Expand your search, consider ‘fixer-uppers,’ and utilize an expert real estate agent for market insights. |

| Alternative Paths | Look into co-buying, tiny homes, house hacking, or rent-to-own options for varied entry points. |

Frequently Asked Questions About 2026 Homeownership

The projected 7% price hike in 2026 is largely driven by a persistent imbalance between housing supply and demand, coupled with ongoing inflationary pressures and rising construction costs. Additionally, strong demographic trends with more people entering prime home-buying ages contribute to increased competition.

To improve mortgage chances, focus on boosting your credit score by paying bills on time and reducing debt. Lowering your debt-to-income ratio is also crucial. Getting pre-approved for a mortgage before house hunting demonstrates serious intent to sellers and lenders.

Yes, many federal, state, and local programs offer assistance. These include FHA loans, VA loans, USDA loans, and various down payment assistance programs (DPAs). Eligibility varies, so researching options specific to your area and income level is highly recommended.

In a seller’s market, effective negotiation strategies include being pre-approved, offering flexible closing dates, and limiting contingencies where possible. A competitive, but not reckless, offer is key. Working with an experienced local real estate agent can provide a significant advantage in crafting an appealing proposal.

Absolutely. Given the challenging market, exploring alternatives like co-buying, tiny homes, house hacking (buying a multi-unit property), or rent-to-own programs can offer more accessible paths to homeownership. These options can significantly reduce upfront costs and monthly expenses, making homeownership more attainable.

Conclusion

Navigating the 2026 housing affordability crisis, with its projected 7% price hike, will undoubtedly test the resolve of first-time buyers. However, with a clear understanding of market dynamics, meticulous financial planning, and a willingness to explore both conventional and alternative strategies, homeownership remains an achievable goal. By leveraging government assistance, adopting smart property search and negotiation tactics, and committing to long-term financial stability, aspiring homeowners can transform challenges into opportunities. The path may be demanding, but with informed decisions and strategic action, the dream of owning a home in the United States can still become a reality.